Why the battery market must be accelerated

After years of progressive increase in residential market uptake of Energy Storage Systems (ESS), some market players have suggested we have exhausted the early adopters and are into the next stage of market maturity. That’s understandable, as first purchasers of home batteries were either wealthy buying brand-name batteries, or subsidy-driven buying the lowest priced option; now market demographics have changed to ‘middle Australia’.However, by definition the first 2.5% of the market is Innovators; the next 13.5% are Early Adopters, then the next 34% are the Early Majority. With one-third of homes hosting a PV system, the PV market is in the Early Majority phase; if you exclude apartments and renters then the PV market is more appropriately in the Late Majority phase for home-owners.

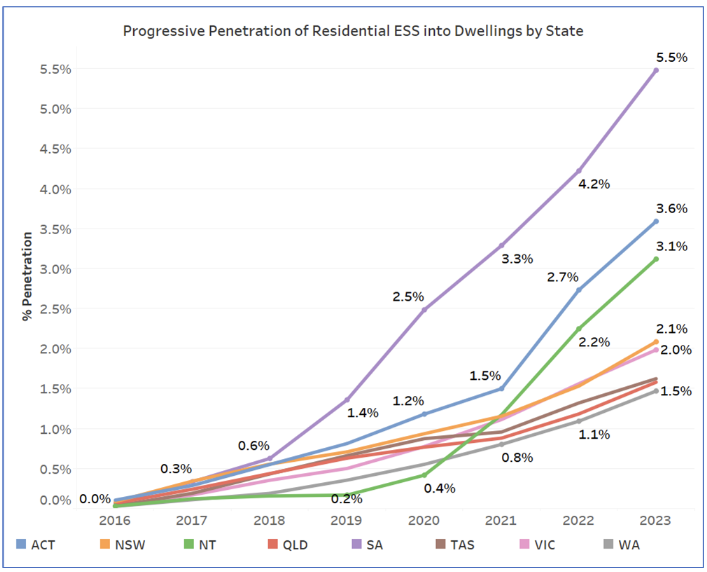

As with all things, there’s considerable variation by state. South Australia was a long-time leader in battery deployment, and crossed the Early Adopter threshold in 2020. ACT followed in 2022, and the NT in 2023 (with a stunning attachment rate over 50%). But the most populous states are still below 2.5% penetration, as is the national average. Adjusting these factors for home ownership pushes them all into Early Adopter territory, but still falls well short of Early Majority.

– SunWiz

Considering all the benefits batteries can bring when people can afford them, it’s time for a national subsidy.

Much more information on Customer Demographics and Consumer Interest is contained in the 2024 SunWiz Annual Battery Market Report. See battery-market-report-australia-2024/ to download a sample.