How to gain and secure market share for your equipment brand

Over recent years, solar panel and inverter manufacturers’ supply chains have been impacted by the global pandemic with brands competing at greater intensity. There’s just no way about it, business conduct has undergone dramatic changes. And some solar participants can no longer justify their operations.

Industry titan – LG Energy – a subsidiary of the LG Group has recently announced its exit from manufacturing solar panel products to “…focus on other businesses that will provide new experiences and value” to their customers. While another source quotes “…rising material costs, supply chain constraints, and intensified price competition”.

LG Electronics Australia will continue to provide warranty and after sales support on prior purchases but will no longer manufacture the products Australian retailers have come to know and rely upon.

BUT… Could they have increased and held greater market share?

SunWiz’s MarketView (Panels) report – which relies on anonymised retailer’s account level data – indicates LG Energy held 5% market share for the month of January 2022 (7% over 2021) and ranked equal ninth nationally. The relative size amongst quality panel players can also be seen in the right chart, which shows LG held a leading but not dominant position amongst manufacturers of top-quality panels.

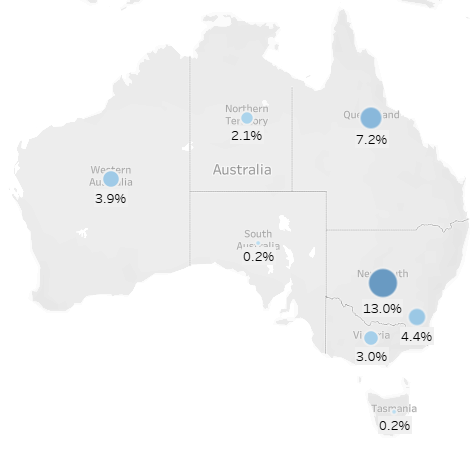

LG was strongest in NSW (over the last 12 months – date ending January 2022), where it held 13% market share. It was weakest in SA & TAS where it was barely represented. This may be because their corporate office is in NSW as well as stronger distribution channels.

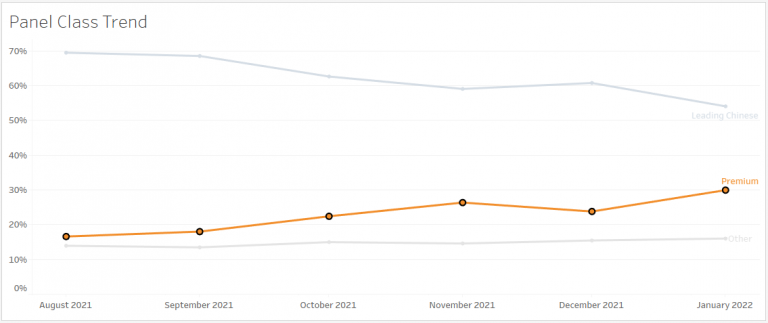

LG didn’t cease global manufacturing because it was performing poorly (in terms of market share) in Australia; quite to the contrary. Amongst manufacturers of quality panel manufacturers, LG held the leading share. On top of this, there was a trend in Australia towards premium-quality panels, which now make up 30% of the rooftop market (as illustrated below).

But with LG’s market share over recent months fluctuating within the 4-6% range and two other panel manufacturers closing in on LG’s position, could the brand have solely relied upon its brand reputation and quality of its products to stay competitive?

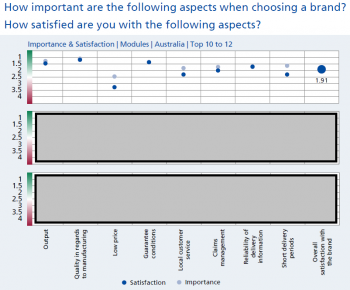

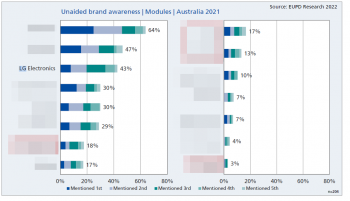

Well, the answer is not so simple. For example, the InstallerMonitor 2021/2022 report published by EUPD Research in cooperation with SunWiz shows that despite retailers’ high levels of awareness of LG’s products – ranking it 3rd – highest overall and highest amongst quality providers (red blurs in left image), LG’s users were dissatisfied with the panels pricing and procurement options (right pane).

That said, LG was still popular when compared to most solar brands, given a healthy Net Promoter Score (NPS) by installers/retailers, an NPS that was 4th best in the market. However, all the brands that had a higher NPS than LG were its direct competitors – manufacturers of top-quality panels. So, while being liked, perhaps it wasn’t liked enough.

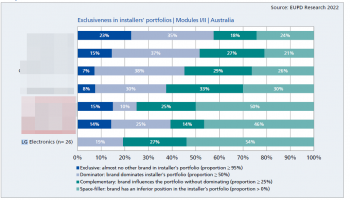

Despite their strong brand name, plus the degree they went to communicate their quality, and high levels of support for their dealers, LG couldn’t command a large share of their customers’ (retailers) business. This is evidenced by the InstallerMonitor charts on degree of exclusiveness in installers’ portfolio. LG ranked middle of the road for installer loyalty, with over 50% of its customers only performing the occasional job with it, and with no survey respondents stating they used LG exclusively. This contrasts with other quality manufacturers (red blurred areas) which had customers that used their panels exclusively or for most of their installations.

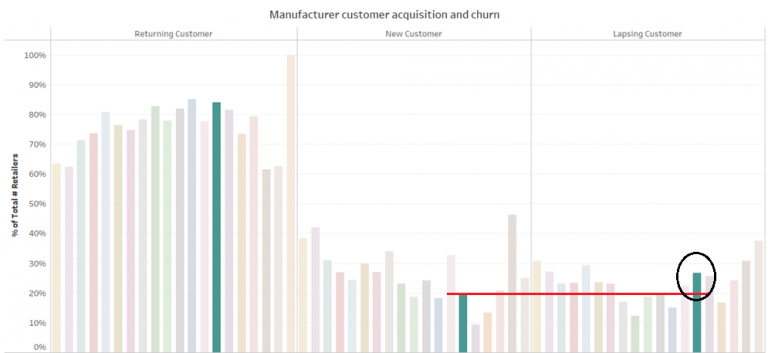

This is further evident in our MarketView report, which looks at the share of a retailer’s wallet which goes to a given brand. LG is the teal circle in the next chart, which shows despite their high volume (vertical axis), the share of wallet for a typical customer (retailer) was only 7%. This contrasts with some smaller providers who captured 60% of their typical customer’s business. SO although LG had the highest volume throughput amongst quality brands they ranked last in terms of capturing share of retailer’s wallet.

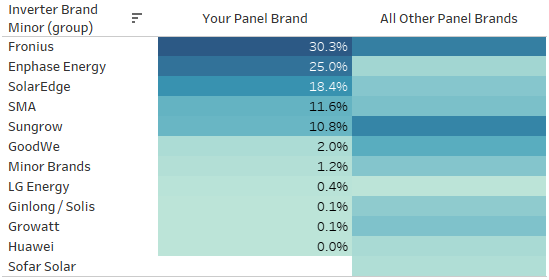

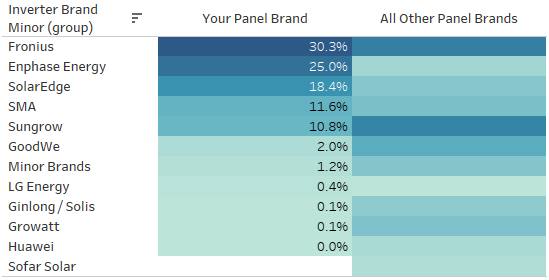

Lastly, understanding which companion products are coupled with a given brand allow for better co-branded marketing. In this case LG tends to be coupled with European & Module-Level Power Electronic inverters. For example, the strong pairing with Fronius implies that many of the systems being demanded are of a high quality.

So, could LG have leveraged the quality of their products to drive a greater number of sales?

Although many customers were aware of the brand, poor segmentation and targeting, supply chain issues and high prices all contributed to increased levels of churn within the brand and as a result acted as a deterrent to many retailers. If LG Energy could have continued to innovate on the ways it sought to deliver value the price premium or more so their margins would have been justifiable.

Interested in your own panel or inverter brand’s analysis? Consider how similar analysis could identify how your market share is evolving, compared to that of your direct competitors, within the context of your market segment. Plus understand how you’re seen by the market and what you can do to improve customer perceptions and loyalty.

- What’s your past position, where are you now, in which direction are you heading?

- How does that compare to your competitors?

- Where are your strengths and weaknesses?

- What’s your share of wallet? Your typical customer size?

- How does that compare?

- Are you churning through customers (retailers)?

- How do your customers view you

- How do your customers view your channels to market

The InstallerMonitor Report answers:

- Appraise similar information for your wholesale distribution channels

- Brand Awareness

- Customer volume

- Exclusivity

- NPS

- How well they meet multi-factor customer satisfaction expectations