The battery market size is higher than many people realise

The question SunWiz gets asked most these days is “How big is the battery market”.

That’s a question that’s perfectly understandable.

After all, there is a government database that accurately tracks the the PV market – but there’s no equivalent data source for batteries.

Whereas we regularly identify ‘missing’ commercial solar systems from aerial imagery, you can’t see batteries from airplanes.

In the face of such market opacity, many rely upon the government data sources that do exist, little realising that they are capture segments of the market and are incomplete at doing that. Hence people’s confusion or surprise when SunWiz announces the market is much bigger than those data sources suggest.

TLDR

- Government datasources routinely under-report the market size:

- The DER Register: ESS installations in 2022: 15941 installations

- CER data on concurrent PV & ESS installations: 20457 installations

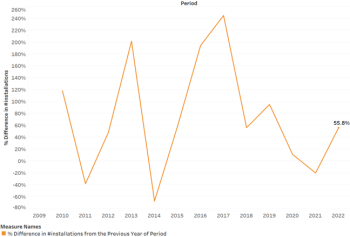

- Government data sources confirm 55% growth occurred in 2022. 55% growth on SunWiz’s 2021 figures is 46,881 installations.

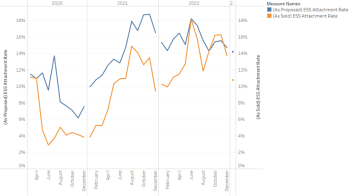

- Proposal software points towards a 15% attachment rate in 2022. This infers a market size of 47,100 installations.

- Manufacturer claims (adjusted by SunWiz to reflect numerous market share datasources) point towards the same market size

Concurrent installations of batteries and PV: The Clean Energy Regulator

The CER publishes data that captures information about concurrent installations of batteries and PV. In 2022 there were 20457 such installations recorded.

On the STC-registration forms there is a checkbox installers can tick to indicate a battery is being installed at the same time as the PV system. Whereas most of the information that’s captured on the STC form is essential, this one checkbox isn’t hugely reliable: its voluntary to fill in, it signifies intent to install a battery but not certainty a battery was installed, and there are no penalties for incorrectly filling it in.

The key limitation of this datasource is it doesn’t capture the battery retrofit market. Because it only captures batteries that are installed at the same time as a new/expanded/replaced PV system, it doesn’t capture batteries retrofit to PV systems that are unchanged – and retrofits comprise about one-third of the market.

Despite that, the CER data provides useful information on trends that are occurring in the market at a national and state level. While the absolute figures can’t be relied upon to be 100% accurate, relative to previous years the figures illustrate changes in the market that are valuable to understand. For instance the CER figures point to a 55% growth in the battery market in 2022.

Separately, the CER shines a invaluable light on the degree to which PV systems are being replaced or expanded when a battery is added. This information clearly points to a grey-zone between retrofit and new-build batteries, which helps manufacturers develop products that meet the needs of the market.

State government data

The Victorian and South Australian governments had the largest battery subsidy schemes in 2022. Each provides data on how many battery subsidies were taken up. That information can’t answer how many batteries were installed nationally, but it provides a helpful clue to local conditions, with one major caveat. Those state government schemes don’t cover the entire market even within their state. The Victorian subsidy is limited to households with income below $180k/year, plus some other constraints. The SA subsidy was more widely available, but doesn’t include installations that occurred in the SA VPP.

Despite their limitations, the state government datasets help to understand the degree to which battery systems are retrofit to existing PV systems – and understandably SA has a high retrofit rate due to its high-penetration of PV. The datasets are also helpful in identifying how battery size differs when retrofit or new-build. We are incredibly grateful to the state governments for all the data they provide as it builds a richer understanding of the market.

Distributed Energy Resource Register (DERR)

AEMO operates the DERR, which collates information on the number and characteristics of DER including PV and ESS. The DERR recorded 15,941 installations in 2022.

It was hoped that the DERR coverage of the ESS market would be conclusive, and remove the need for any guesswork about battery market size. Indeed many companies point to the DERR data as being the source of truth on battery market size.

However, people must understand the limitations of the DER Register:

- It only collects information on grid-connected batteries.

- It only covers the NEM and WEM.

- It relies upon installers submitting information to DNSPs.

- In NSW, it relies upon installers submitting information directly to the DERR.

Installers should be notifying DNSPs when a battery is added to the grid. That doesn’t always occur, particularly in the case of a battery retrofit. Using half-hourly household energy consumption data, DNSPs have performed data analysis that identifies that ‘fingerprint’ of a battery – presumably exporting power only in the afternoon, with dampened grid demand through the early evening. In doing so, they’ve seen plenty of occasions where DNSPs weren’t notified of battery installations.

The DERR relies upon installers submitting information to DNSPs, but NSW DNSPs don’t upload information to the DERR but instead expect installers to do so directly. Whereas installers face penalties for not advising DNSPs of a battery installation (clearly not all installers are aware of this), there are no such penalties if they don’t upload information to the DERR. As a consequence, NSW is horribly under-represented in the DERR.

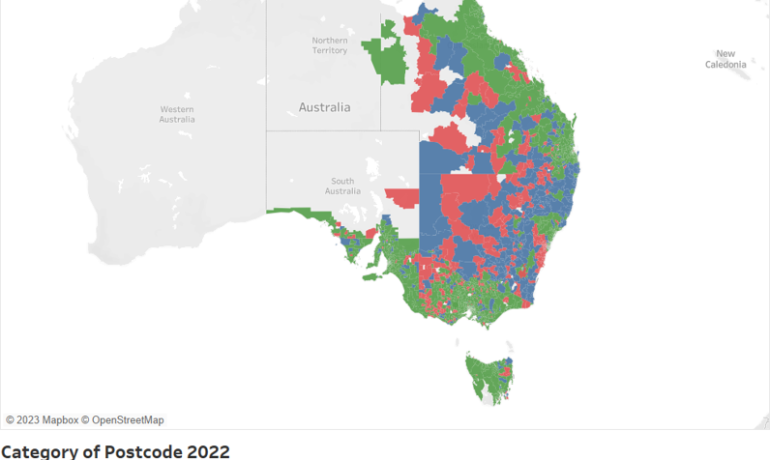

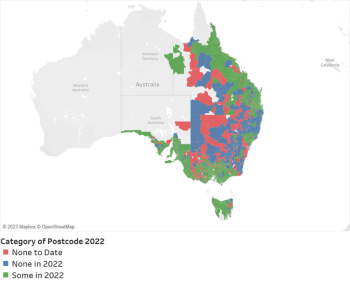

This chart illustrates the most important shortcoming of the DERR: the clear underreporting of ESS installations in NSW. The chart illustrates vast swathes of the state have never had a battery installed, and plenty more that had no batteries installed in 2022 despite reporting battery installations in previous years. NSW is the sole state where this happens with such high frequency, which is concerning as other data sources (including CER data) point to NSW being one of the largest markets in the country.

AEMO provided SunWiz with a statement “We are aware that the number of batteries reported in the DER Register I swell below what is understood to be installed. We are currently engaging with DNSPs to improve the collection of battery information, and we expect that more robust collection processes will also develop through work being done to collect EVSE information in the DER Register.”As a result of these limitations and demonstrated shortcomings, the DERR cannot be relied upon for absolute figures, particularly when those figures are lower than those of the CER, which itself is a sub-set of the total market. But the DERR’s relative figures highlight valuable trends. Such as a 55% increase in ESS deployment in 2023 compared to 2022. The same growth rate as seen in CER data.

So how can market size be reliably calculated?

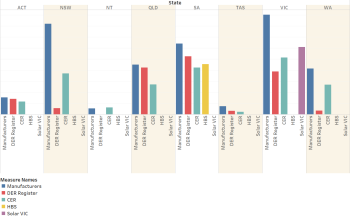

Its only when you combine all the different data sources together that the hidden richness of the market is revealed. The picture below reveals the comparatively-healthy reporting that happens in South Australia, Queensland and the ACT. But there are stark differences between figures reported by the various datasources in NSW & WA, and (to a lesser extent) Victoria.

The 2023 Annual SunWiz Australian Battery Report covers all of this in so much detail, with over 200 slides of content essential to the success of market participants.Learn more about it here.