Solar Industry Report Card – 2014

If the life of a child named “Sunny” was used as an analogy for the Australian Solar Industry, 2008 would be the birth. 2009-2011 would represent its infant years of fits and starts, growth spurts, testing its independence from its governmental parents. 2012 was the year of wild excitement that a 4-year-old enjoys before the reality of attending school hit in 2013. But after studying hard, 2014 can be viewed as the year that “Sunny” finally started to grow up.

So, what lessons can be learned for 2015? A lot is revealed by “Sunny’s” 2014 Report Card.

Mathematics

Sunny is great with numbers, and has slightly improved upon last year’s efforts. Though Sunny once had difficulty counting past two, this year his favourite number was three, and five was his second favourite number. This year Sunny managed to count to one hundred on 207 occasions, and Sunny is tackling bigger and bigger numbers.

SunWiz’s calculations (based upon projections from incomplete data) show there was 825 MW of sub-100kW PV installed in 2014, a slight growth on 2013’s 810MW. Importantly, there were 187,000 systems, a 8% decrease on 2013, which signals a declining residential market that will be concerning for anyone without a commercial focus. Consequently, the average system size grew to reach 4.8 kW by year’s end, but even residential systems got bigger. 21% of the market exceeded 8kW in 2014, and there were 207 systems of 100kW in size installed in 2014.

Geography

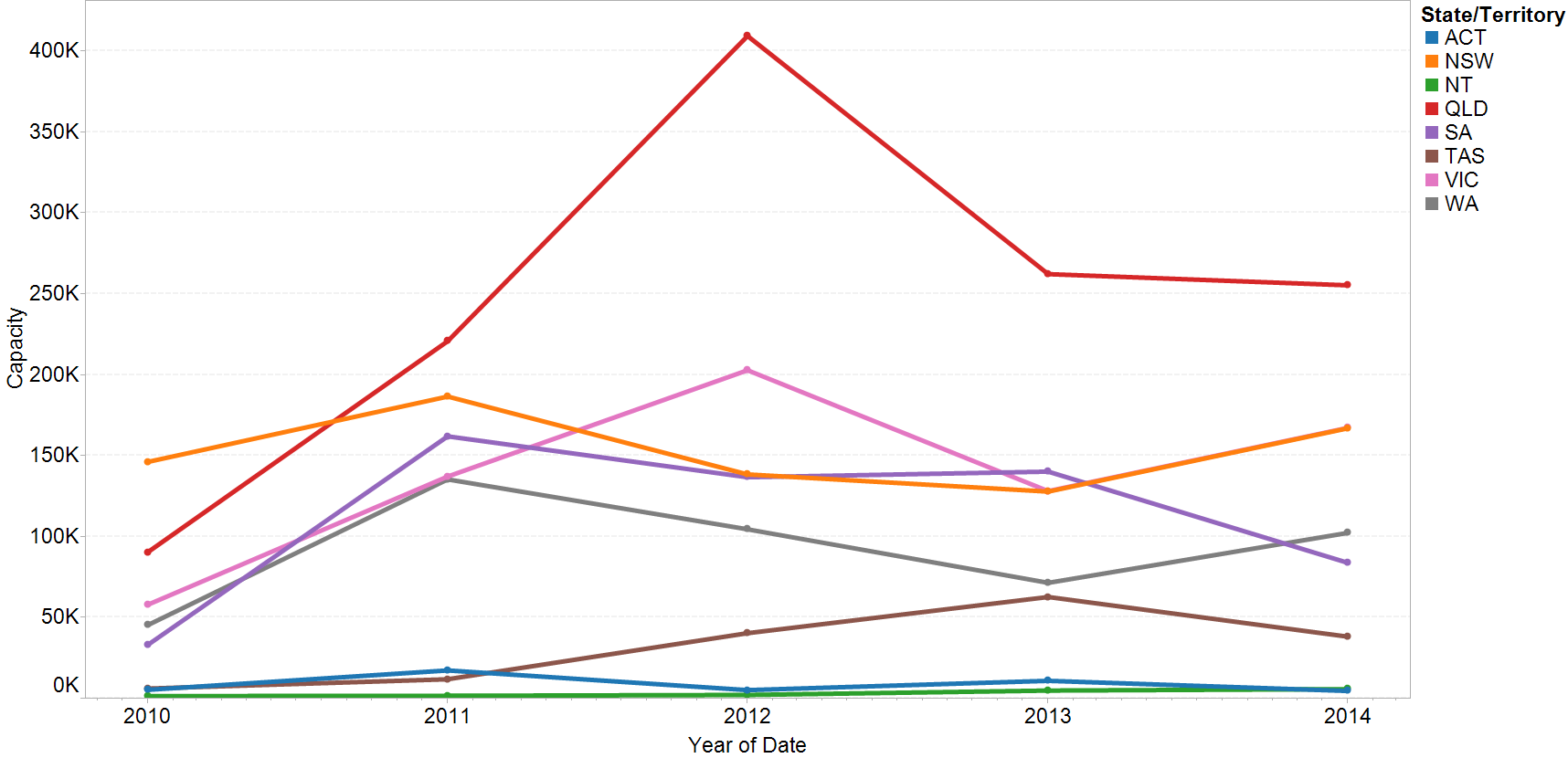

Sunny’s geography knows no bounds. Sunny has enthusiastically reached into every corner of the continent, and yet he has his favourite places. Queensland is his favourite state, and he can’t decide between New South Wales or Victoria as his second favourite. South Australia has fallen from favour in preference for Western Australia. Sunny’s #1 playmate was Mackay

Postcode 4740 (Mackay) was the #1 location for installations in 2014, adding 5.9MW worth. 7 of the top 10 postcodes in 2014 were in Queensland; 2 were in WA and 1 in Victoria. Statewide, Queensland’s 2014 figures were practically level with 2013; NSW and Victoria had the same figures in 2014 and in 2013, thus both enjoyed substantial growth. South Australia contracted dramatically, and was overtaken by WA which grew considerably.

Economics

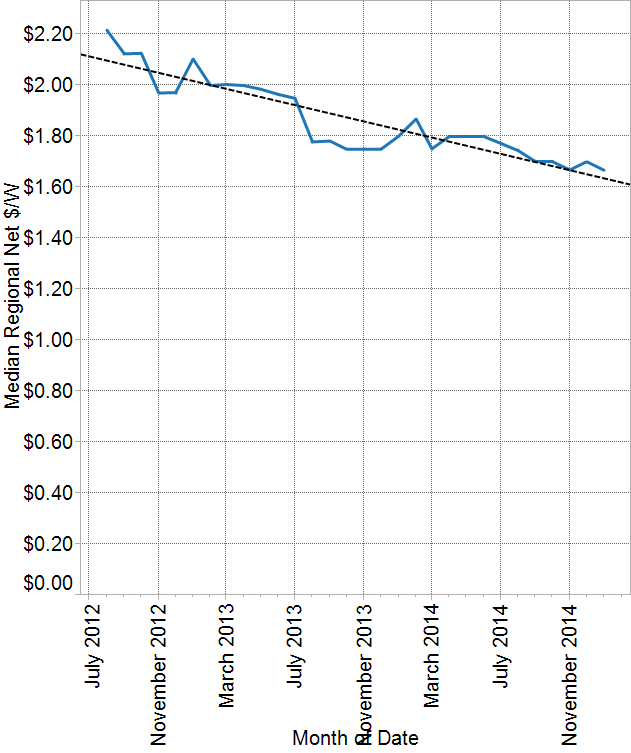

Sunny is excelling at economics. Somehow he manages to continue to decrease cost month on month, little by little, setting record low prices in the process. However, Sunny may be doing so at the expense of sustainable profitability, and could come unstuck if caught out by external factors such as the Australian Dollar or Anti-Dumping Commission. Sunny’s presentation of financial calculations falls well short of where it needs to be, though calculators are available and accessible.

The graph below shows the evolution of system pricing, according to Solar Choice’s price database. There has been a decline in Net System price (after STC discount) each month, only some of which has been due to the increase in STC price over the first 18 months displayed.

English and Communication

Sunny’s attempts at communicating with his elders lack maturity and sophistication. Though he was everyone’s darling when born, he has more recently reacted with rebellious language to the withdrawal of affection. Sunny is making enemies amongst his teachers and will not be invited to the party unless he changes the tone of his conversation. Despite this, Sunny has made many friends amongst his peers and looks like he may lead a rebellious coup that may well be successful.

Though the government’s RET Review has yet to reach a conclusion, the government has stated that there will be no changes to household solar entitlements, and that 100kW systems will remain in the SRES. Despite this, the SRES is not completely safe, but appears to be taking a back seat in negotiations that are focused upon the major point of difference between the major parties – the GWh figure of the LRET. In 2014 SunWiz met with MPS and government representatives as part of the RET Review, as part of contribution to Solar Citizens, Australian Solar Council, and the CEC’s PV Leadership Committee and Domestic PV Directorate (of which Warwick is the Chair).

Dance

Sunny has incredible internal dynamism, and while his expression appears on the surface to be stable, beneath the surface he exhibits huge internal motion. The dance of Sunny’s inner world appears hell-bent on creative destruction as his major and minor organs battle one another for energy. It is quite likely that this will result in injury to certain body parts which will hopefully not cause Sunny to meltdown.

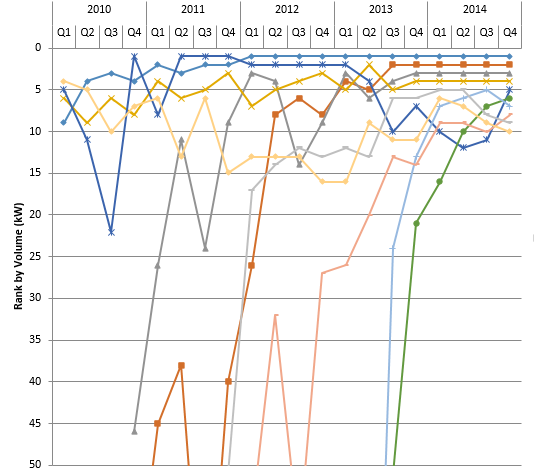

The ranks continue to be dynamic. Origin started off the year as the 10th biggest PV retailer, and ended up as the 5th largest. True Value Solar retained position #1, though faces increasing pressure. The top 10 features two companies which only started to create STCs in 2013. The graph below shows the shift in the ranks of the current top 10 non-aggregating STC creators.

Science

Science is perhaps Sunny’s weak point. Too often Sunny appears to guess the answer to questions such as “how much of the generated solar power will be exported” and consequently his answers to “how quick the payback be” are misleadingly fast. Sunny has learned the merits of using computers to improve the accuracy of his answers.

Some export figures from analysis has shown that the median 1.5 kW system exports 37% of its production, but most systems sold these days are 3 or 5 kW, which have median export volumes of 60% and 74% respectively[1]. SunWiz will be launching a free solar export calculator to assist the customers and players in the solar industry to access more accurate information about likely export volumes.

Health and Physical Education

Sunny excels in outdoor activity. He leads his classmates in speed of installation, but has a tendency to cut corners. His quick-fix diet of fast food in earlier years has not prepared him well to tighten his belt for the occasional fasting that is required in recent leaner years. Sunny runs on the spot far too often and could improve his effectiveness by working smarter, not harder.

History

Sunny is showing a blatant disregard for his predecessors. But if history has anything to teach Sunny, its in understanding the patterns of his own growth, and accelerating his focus upon these areas. Sunny has amassed a huge amount of experience which can now tell him which businesses in which locations to target for highest-profit sales. Sunny has collaborated with his classmates to coalesce their common knowledge, which will enable them to beat their common foe.

Tips for a Sunny 2015

Sunny has a knack for responding to the opportunities that present themselves. However, 2015 will present new challenges for Sunny as classroom dynamics, schoolyard bullying, misbehaving masters, and declining territory all gang up on him. Sunny has his first major stint on the solar farm this year which is expected to contribute to a bumper harvest.

In its entirety, I expect 2015 will have good volume that may well exceed that of 2014. The utility-scale sector will set records this year, as Flagships, Moree, Mugga Lane & OneSun are delivered…. and then you’ve got projects like Rio Tinto Weipa, Majura Park, Coober Pedy and other ARENA projects, plus CEFC investments. Unfortunately, most of the 3000+ Australian solar business will be unable to access such utility-scale opportunities, leaving them competing for a residential market that will naturally decline as low-hanging fruit dries up. This makes the commercial sector all the more critical, and businesses will survive only if they crack this market, which offers potentially greater profit margins and value-focussed competition. But for the majority of the industry it will be a scramble to sell whatever residential systems they can to keep cashflow going while they chase bigger dreams of upskilling and upscaling their commercial activities.

Extraordinary offer: Our 2014 market wrap edition of Insights is available for a special deal until Friday 30th of January. Typically we don’t sell individual editions, but this one is too good to withhold. Learn:

- The installation volume of each the top 20 companies and how it has changed over the past year.

- The most successful companies in commercial PV, and how they’ve got there

- The top 10 locations for PV in 2014… the best places in 2015

- Where most commercial PV volume was installed, and by whom

- Which system sizes helped drive market share in 2015 and their critical importance for 2014

- How to price your system competitively for a range of different panel-inverter combinations

- Plus much more from our regular Insights content

The special edition is available at a price of $950 ex GST, or it included with six months worth of updates for $1650 ex GST.Click here for more information.

SunWiz’s latest activities

In the past months we’ve been:

- Launching an incredible service that helps companies improve the profitability of small commercial sales

- Developing a web-database of commercial PV projects

- Re-developing PVsell and packing it with new features

- Representing Australia in Kyoto for the International Energy Agency’s PV Power program

- Advising a business that to reduce proposed installation sizes from 30kW back down to 5-10kW on a number of sites.

- Comparing the financial return from PV and SHW

- Developing a battery energy and finance model

- Getting engaged in Malta and touring through Europe, including looking at the Vatican’s Solar Array