Solar Industry Snapshot and Directions

I was to give a presentation to the SEIA Queensland seminar but wasn’t able due to illness. Rather than let the intel go to waste, here it is as a blog post.

- Solar businesses are feeling the pain

- Volumes are down, but not enough players have left the market

- So Price competition is intense, eroding profit margin

- Lower volume at lower profit = maximum pain

- If you’re feeling this way, you’re not alone… in fact most of Queensland is in the doldrums, as you’ll see from this presentation

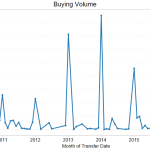

What the F*** just happened, queensland?

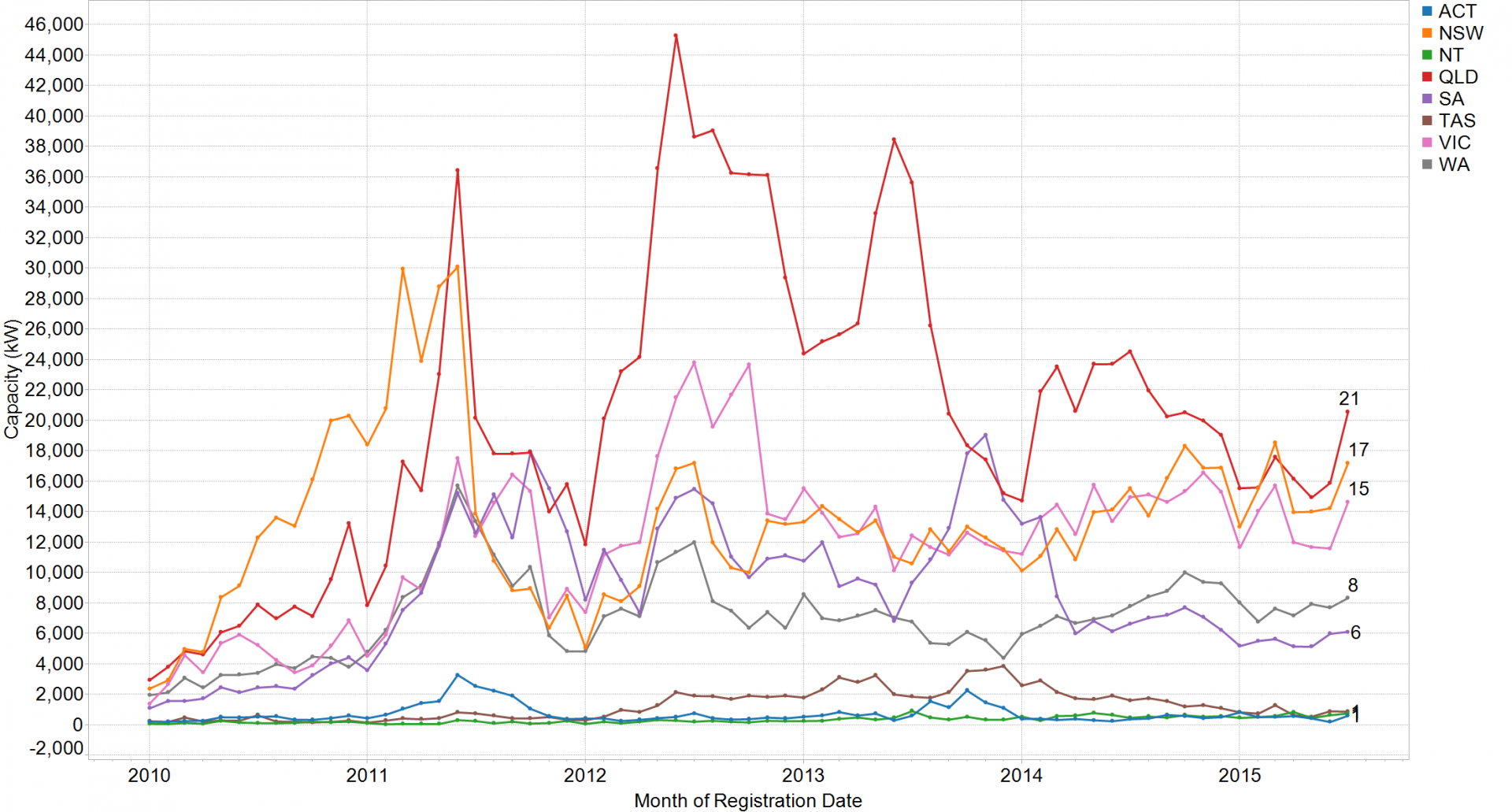

This chart shows just how bad things are across Queensland (represented in Red – the chart shows capacity registered in each month. You can see Queensland’s peaks in 2011 and 2012 (solar multiplier reduction), solar bonus scheme ending boom 2013. In 2014 volumes fell right back but were still propped up a little by the 8c/kWh tariff. But 2015 has been a shocker in Queensland. Actually its been poor across most of the country, which has struggled to reach 2014 installation volumes.

July 2015 saw a spike in installation volumes, back to last year’s level. But its too soon to say whether this will be sustained or was a one-off.

Either way, it’s a situation of low volume high-competition.

STC Prices

- (I usually get asked about STC price forecasts)….

- National volumes are down 10% on last year

- This has caused a STC undersupply, with $40 available through the clearing house

- This situation will continue through to end October 2015

- From November 2015-February 14 2016 STC price could fall.

- The improving STC price largely offset the fall in the $AUD, so any fall in the STC price will increase system prices, making life tougher.

Have We Reached Solar Saturation?

- One of the challenges is the ever-diminishing number of houses left without solar. Increasingly those left are sub-optimal, with poor paybacks.

- This chart shows the penetration of solar into suitable dwellings (owner occupied, detached/semi-detached). Grey = 40-60% penetration, and Red = >60% penetration.

- You can see there are large swathes where solar has reached most of the suitable customers.

- Your job is to convince customers who haven’t decided to do solar before when there was a FiT that now is a good time

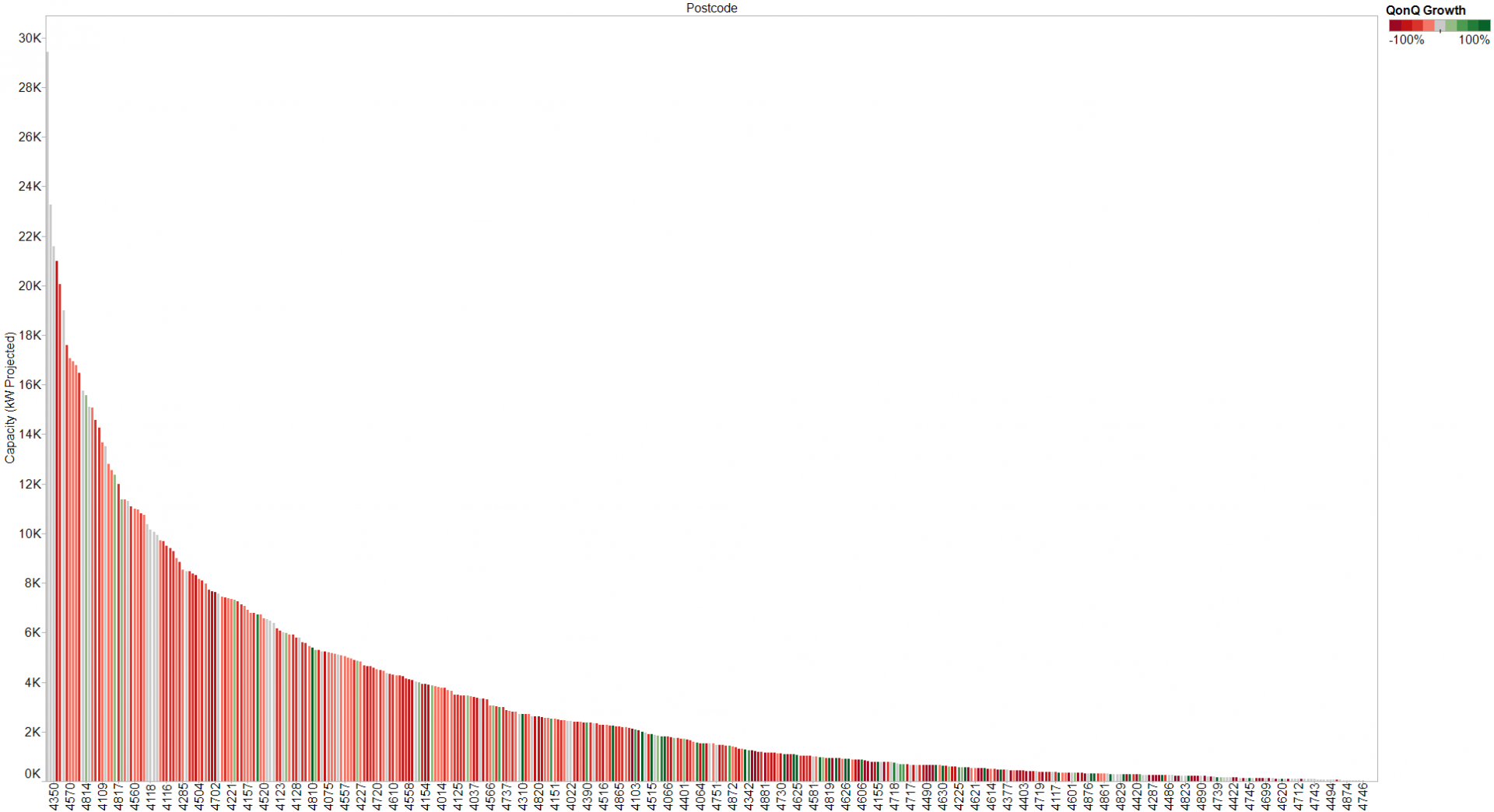

Important trends: Queensland Market decline

This chart (below) shows the amount of volume ever installed (vertical axis) for each postcode (horizontal axis), with colour indicating the growth in the most recent quarter (compared to the previous quarter).

You can see that most postcodes are red, indicating that they are contracting.

Some are stable – particularly those where a lot of PV has historically gone in. But very few are green indicating they are growing. Those that are growing typically have smaller volumes, so may not be of such interest.

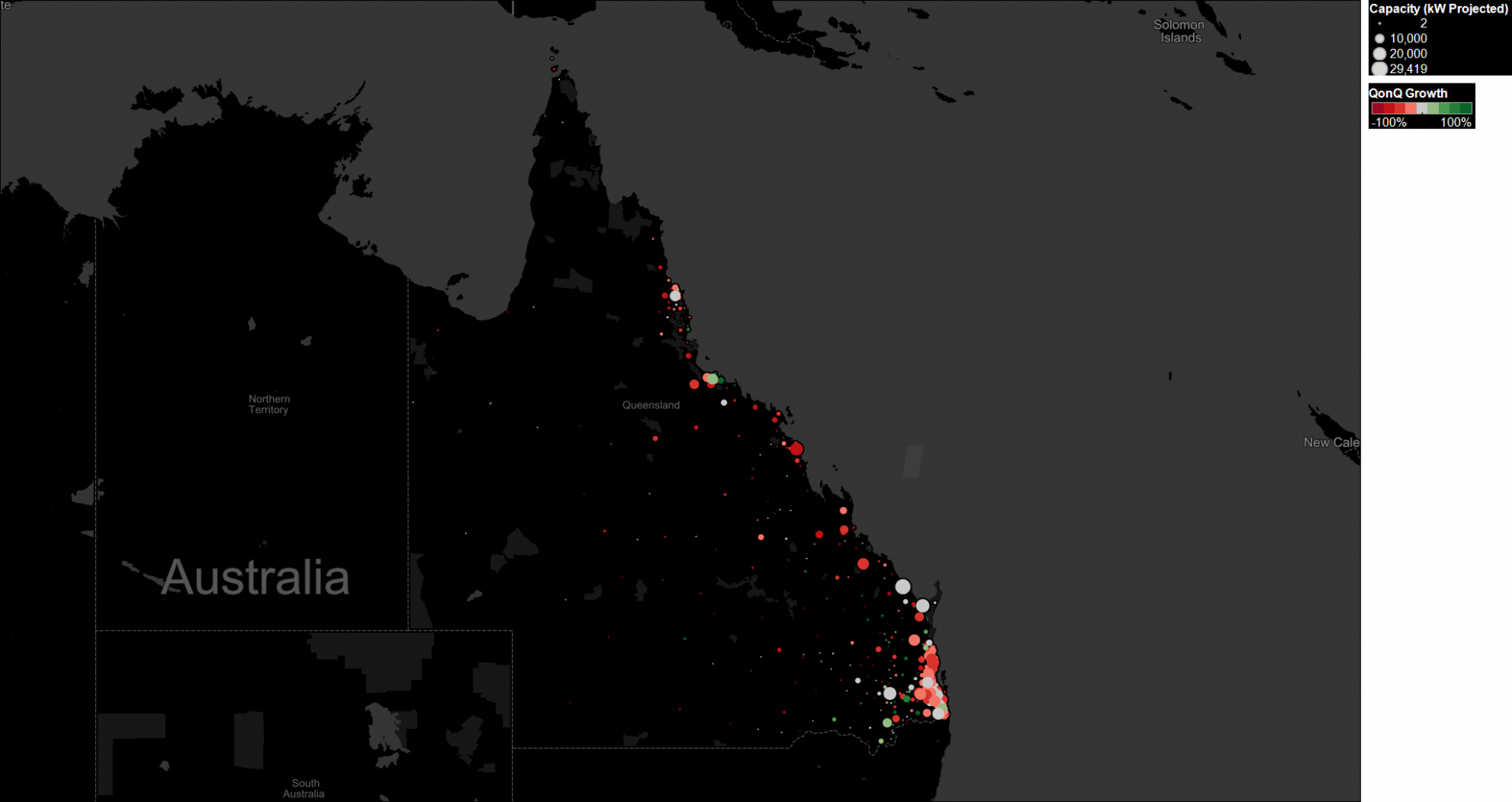

Important trends: Queensland market decline

This map shows the same information, plotted geographically. There are some growth areas in south-east Queensland and around Townsville, some areas of stability on the Sunshine Coast, Cairns, and the Gold Coast, but most places are contracting. Targeting the growth areas is a sensible business practice.

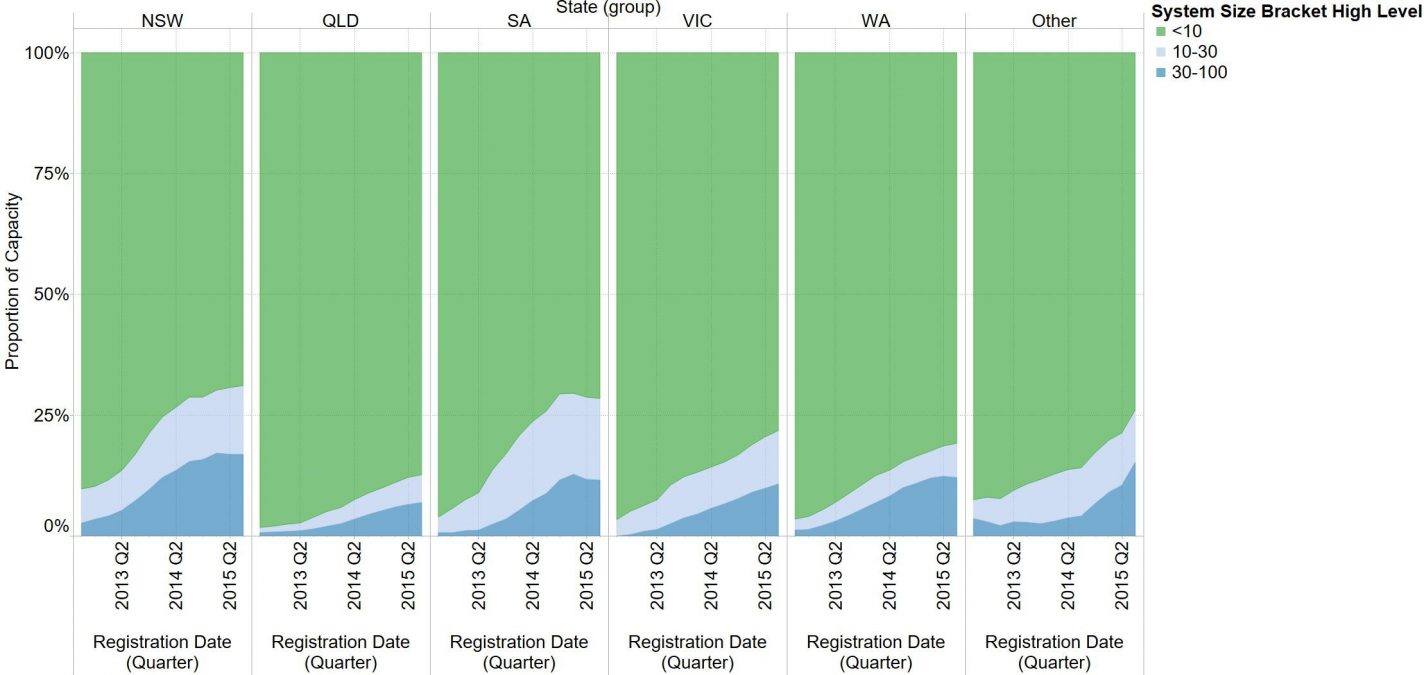

Important trends: Commercial progress… lagging behind in QLD

- The chart below shows the evoloution of the proportion of the market in the residential (green), small commercial (light blue) and medium commercial (dark blue) segments, for each state over the past year.

- Counter to the rest of the country, Queensland has seen a low volume of commercial installations

- At 10% market share, Queensland Commercial is half the national average and one third of NSW and SA’s proportion of commercial

- Commercial represents a major opportunity for Queensland, however unbundled commercial electricity prices (for large consumers) are lower here than anywhere else in the country.

- The opportunity here lies in actively reduction peak demand with batteries and load management combined with solar.

- The other opportunity is small commercial installations.

Important Trends: Tariffs

Ergon is making tariffs more complex, which will make it more difficult to calculate financial benefit

· Tariff 11: 24c/kWh 117c/day

· Tariff 12: 52/19 c/kWh (summer) +129 c/day

· Queensland has some of the lowest unbundled (commercial) electricity prices

· Moving towards peak demand charge (average of customers top 4 demand days in the month)

o 3pm-9:30pm summer residential

o 10am-8pm summer weekdays commercial

o Minimum 3kW demand charge

· Q: How will you calculate your financial benefit?

Important trends: Ergon’s Network Connection impact

- Ergon is also requiring export limitation or non-unity power factor

- Your CEC/STC-required performance estimate must account for this:

- Export limitation

- Power factor

- Oversized arrays

- !: Sign of things to come nationally

- Q: How are you accounting for this in your financial calculation?

- (PVsell will handle all of this in a forthcoming release)

What will save our solar?

- Batteries?

- Not yet: need a big differential between Peak/export

- Best case scenario 7 years in limited circumstances in Ausgrid/SA

- Perhaps with demand fees (commercial), but which residential customers will switch to demand charges with 3kW minimum?

- Still, an profitable early adopter market

- PV – electric Hot Water? Be careful of consuming more at Tariff 11 than you avoid in exports

- Upgrades / Retrofits

- Be mindful that you cannot claim STCs on upgrades to old inverters

- PPAs? Haven’t proved to be widely successful yet.

- Definitely a market for servicing, but beware upgrades on old inverters unlikely to attract STCs – cheaper to replace inverter?

- Rental/Units – whoever can win this market will have an unbeatable business model

For the future

- Ergon is trialling PV-storage with SunPower (4.9kW PV & 12 kWh storage on 33 QLD homes)

- Ergon says 20 systems of 100kWh will be deployed in 2015 through S&C Electric Company

- Ergon plans to install 200MW of PV (EOI issued soon + separate tender for 50MW worth of 3MW-10MW to reinforce fringe-of-grid)

- Cook Town: 26MW solar farm & 5 MWh battery courtesy Lyon Infrastructure Developments

- 2GW Bulli Creek solar farm (SolarChoice/SunEdison)

- QLD plans 1600km string of solar powered fast-charging stations for EVs

- Major Utilities anticipated to target QLD for utility-scale rollout (high wholesale prices, growing demand, high solar radiation).

Options from here

- Strategic business consultation: $375 ex GST (2 hours)

- PVsell software: from $650 ex GST per year

- Informedly size systems and accurately calculate export, payback, etc

- Sell more solar by standing out as professional

- Comes pre-loaded with consumption profiles of typical customers

- Over 500 Australian solar companies have produced >12000 proposals with PVsell

- Sign up to PVsell here