10-year Solar PV Installation Forecast for AEMO

SunWiz (supported by Solar Business Services) was commissioned by the Australian Energy Market Operator to produce a forecast of uptake of rooftop PV in NEM connected regions.

Read the forecast below, or download for later reading.

The text of the executive summary is repeated below.

Within Australia, the deployment of solar power has been up until now largely overlooked by parties modelling Australia’s energy mix. However, with over 1.3GW of photovoltaic (PV) solar panels now installed in Australia1

Within a decade, a conservative forecast predicts six gigawatts of solar PV will have been deployed, which could represent 11% of Australia’s generation capacity and over 3% of its electrical energy consumption. Under less conservative assumptions, the Internal Rate of Return (IRR) from residential and small commercial systems are predicted to exceed 15% for most of the coming decade, with IRRs exceeding 25% in all states by 2020 in a more optimistic scenario. At the high end, the installation of 15GW over the next ten years is entirely plausible, and would be equivalent to 30% of forecast generation capacity and 7% of electrical energy production, Australia-wide.

Such levels of installations have the potential to significantly impact Australia’s electricity industry. Issues associated with high levels of low voltage network penetration have already arisen, particularly in long rural feeders. Though technical solutions already exist internationally, without a proactive facilitation strategy by Distribution Network Operators such issues will increase in theirrange. The impact will also be felt by generators and retailers as generation merit order is changed, transported volumes decrease, and peak pricing events alter in their timing and frequency of occurrence.

Deployment of such a large volume of unregistered, non-scheduled generation could present challenges for AEMO. Not all of this capacity will be connected to the NEM, with a large fraction occurring in Western Australia and in remote mines. However, the economics of solar power dictate that the vast majority is expected to be installed ‘behind the meter’, i.e. on premises where solar generation primarily reduces grid consumption – rather than being a dedicated solar generator directly connected to the grid and exporting 100% of its energy. Indeed, it is likely that only a small proportion will be a pure power station exporting, potentially complicating AEMO’s task of energy forecasting.

The impact will also be felt by generators and retailers as generation merit order is changed, transported volumes decrease, and peak pricing events alter in their timing and frequency of occurrence.

Deployment of such a large volume of unregistered, non-scheduled generation could present challenges for AEMO. Not all of this capacity will be connected to the NEM, with a large fraction occurring in Western Australia and in remote mines. However, the economics of solar power dictate that the vast majority is expected to be installed ‘behind the meter’, i.e. on premises where solar generation primarily reduces grid consumption – rather than being a dedicated solar generator directly connected to the grid and exporting 100% of its energy. Indeed, it is likely that only a small proportion will be a pure power station exporting, potentially complicating AEMO’s task of energy forecasting.It should be noted that these scenarios do not represent the extremes – e.g. a ban on PV installations, or a return to premium gross feed-in tariffs.

It should be noted that these scenarios do not represent the extremes – e.g. a ban on PV installations, or a return to premium gross feed-in tariffs.

PV deployment of this scale has the potential to impact many areas of AEMO’s operations in the electricity market. Forecasting and planning will be strongly impacted by PV, which could contribute 50-150% of the forecast growth in generation capacity over the coming ten years

The Economics of the Inevitable . PV is likely to impact upon loss factors, and create additional requirements for Ancillary Services. Dispatch (and its forecasting) will be affected by weather-related factors across a wide area due to the broad swathe of PV installations. Managing a variable non-dispatchable power source will require careful reserve management. PV may impact upon the metering requirements, and particularly in network connections. AEMO’s experience integrating wind power into the NEM will service it well, though there will be major differences with a distributed generation on an equivalent scale.

What drives such levels of deployment? Over the coming years, government policy will continue to contribute a great deal through such actions as the solar multiplier, Solar Flagships, the ACT solar Auction, the Large-scale Renewable Energy Target, and possibly the Clean Energy Finance Corporation. However, these policies merely accelerate deployment of solar, which (due to its economics and simplicity) will in the medium-term will inevitably be popular as a simple way of reducing the high costs of residential and commercial power. Further, the rapid deployment scenario sees solar electricity as being cost competitive with the wholesale price of generation by 2022 when reduced transport losses and time-of-day value are accounted for.

“[US Energy Secretary] Chu’s predictions means that the government’s of the world’s three biggest energy users, China, the US and India, each believe that the cost of utility scale solar will be cheaper than fossil fuels by 2020 at the latest.”8

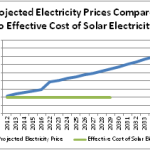

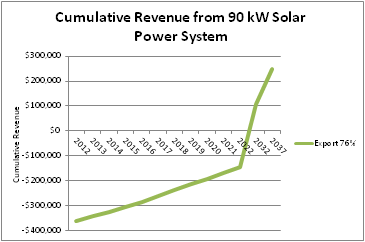

The fundamental drivers of increasingly favourable financial returns for solar power are the ever increasing residential electricity price and the ever-decreasing price of solar power systems.

Figure 4 demonstrates the financial returns available from a 5kW system (assumed to export 50% of its power), under a range of electricity price forecasts. The reduction in solar multiplier and anticipated end to feed-in tariffs notwithstanding, solar power is clearly attractive to the end user.

Slow Uptake: Indeed, it would take a dramatic fall in the Australian Dollar, turnaround in recent trends in electricity prices, breakthrough in other renewable energy technologies, or an act of deliberate market protectionism to withhold Australian PV installations to 6 GW over the next decade. , adjusted for time-of-generation and loss-reduction.

Moderate Uptake: A more likely scenario is steadily increasing demand from the residential and commercial sectors, and a considerable contribution to the RET in its later years, resulting in 10 GW over the coming decade. Such levels of demand could force gentailers to embrace PV, in order to continue to sell energy of some form.

Rapid Uptake: It is well within the realms of possibility that, should current electricity prices trends continue (for any number of reasons), PV being as cheap as wholesale time-of-day power by the end of the decade would result in surging demand for PV on all commercial buildings, households doubling their system size, and CEFC assistance resulting in a previously unthinkable contribution to the RET resulting in 15 GW over the coming decade. With financial returns in all sectors equivalent to those seen in NSW’s solar heyday, such demand for solar would have an unprecedented impact upon the electricity sector – with 30% of standing capacity, solar would have the potential to cause frequent shutdowns of gas turbines.