LGC surrender period

Come the LREC surrender deadline this Wednesday, things are getting tight for power companies to purchase and surrender enough LGCs from the market to meet their liability. Historically, Liable Entities (LE) have had excellent compliance rates, but when the price of LGCs soared last year, ERM and some other LEs opted to pay the shorftfall penalty price rather than surrender LGCs. They were taken to task by the Clean Energy Regulator, and appear to have re-engaged with the market.

This year, there is still plenty sufficient LGCs available on the market to meet this year’s liability – 32.7million are available, and 25.2million need to be surrendered. The problem facing many LEs is that, whereas in previous years LGCs were easy to find as there was a sizeable oversupply, this year some LEs are holding far more than what they need, meaning there are others who must scramble to find LGCs from the market.

There is only three more days for the LEs who don’t currently hold enough LGCs to meet their liability – so they need to quickly discover who is holding excess LGCs, and line up a trade – otherwise they’ll be paying a fine and could suffer reputational damage. But its difficult to know who is holding excess LGCs, as there isn’t a publicly-accessible source of information on who is holding LGCs, how many they’re holding, and how much they have to surrender.

Fortunately, SunWiz has been analysing the REC Registry for 7 years now, and has built up a rich database of information on current holdings, recent years’ surrender volumes, projected 2018 surrender volumes, and trading partners for each Liable Entity. From our RETelligence, we can identify who is holding enough LGCs, and who isn’t.

Here’s some insights we can pull from the data. Note that all of these statements are based off last year’s surrender volumes, adjusted for the increase in the RET target.

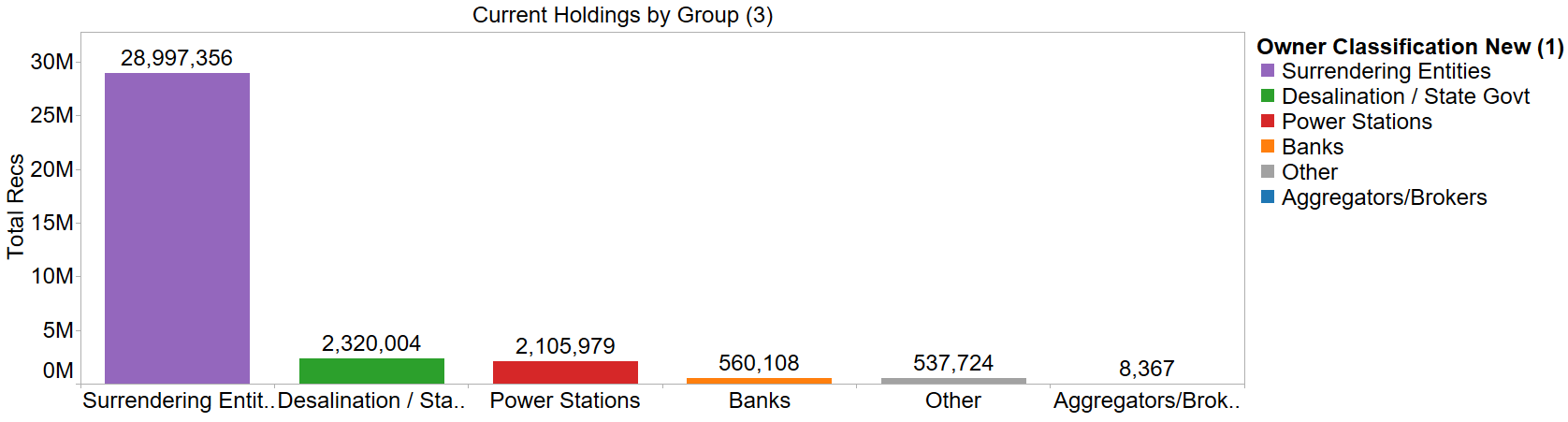

- As a group, the LEs hold sufficient LGCs to meet their collective liability, holding 29M as seen in the chart below

- However, individual LEs appear to hold up to 1M LGCs than their need (e.g. Snowy Hydro).

- Pacific Hydro is holding three times the volume they need for their own requirements. Water Corp is in a similar position, as is Power & Water Corp

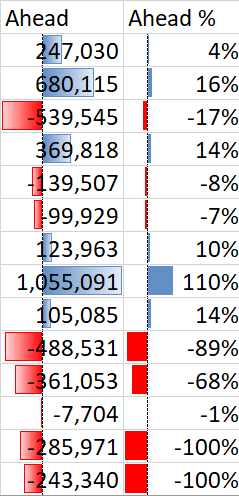

- Other individual LEs are very short, holding up to 500k LGCs less than their Liability with three days left to trade.

- Two of the big three retailers appear to have met their individual liability. The third appears to be 17% short (540k LGCs).

- There are 9 LEs who need to secure 100k or more LGCs in the next three days

Current Holdings by Classification of Owner: LE’s hold 29M at present

Let’s take a look at ERM, as an example.

- ERM is holding 3.2M LGCs at the time of writing.

- Two years ago they surrendered 1.9M LGCs.

- Since then the target has grown from 18.55M LGCs to 26.03M LGCs

- Assuming their market share of electricity sales hasn’t changed in the meanwhile, their liability this year would be 2.67M LGCs

- Therefore they are holding sufficient LGCs to meet their liability.

We can therefore conclude that ERM has met its RET obligation this year.

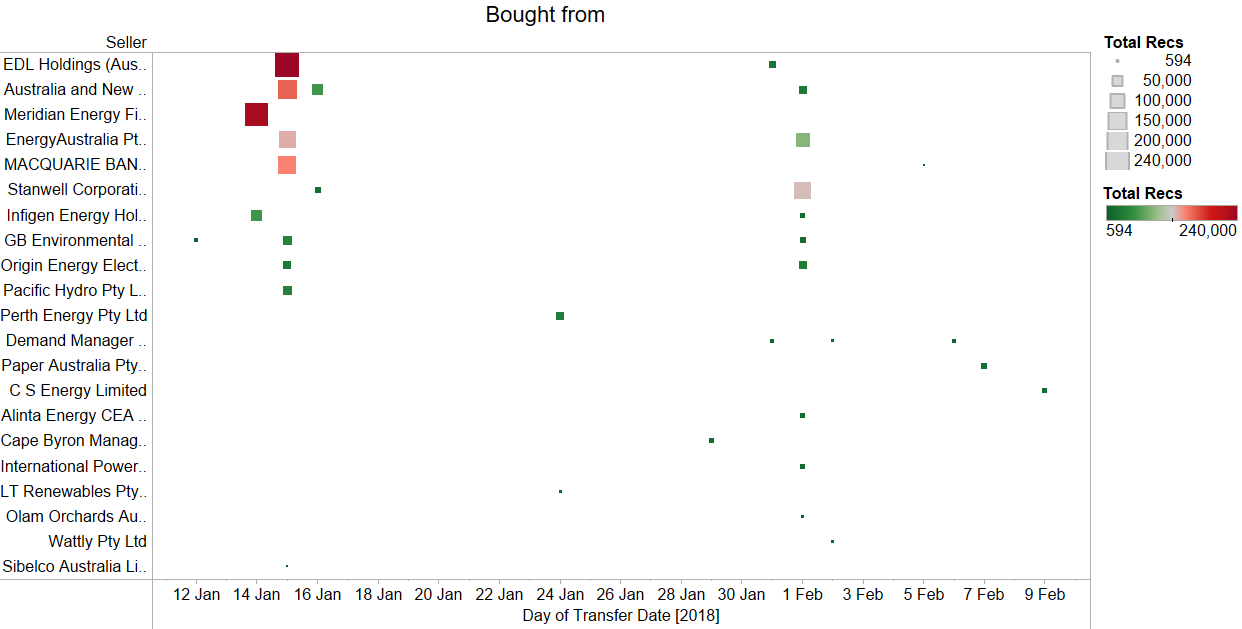

Most of the LGCs ERM bought in 2018 came from EDL, ANZ, Meridian, EA, and Macquarie Bank

But there’s plenty of people who need to get their act together.

- One of the big three, who appear to be 540k behind (17% of their liability)

- Over 16 LEs that still require over 90% of their Liability to be purchased in the next three days.

A small extract of who’s holding more or less than what they need, and this information as a percentage.

If you are a Liable Entity that needs assistance in finding a trading partner in order to meet your LGC liability, please contact SunWiz.