Changing Solar Economics

In an article that featured in the August edition of Solar Australia, industry expert Warwick Johnston – Managing Director of SunWiz Consulting – made some solar pricing predictions.

In the past two years, Australia has witnessed a remarkable solar power price transformation. Driven by a combination of factors including international pricing trends, the favourable exchange rate and the increased deployment of government programs (whose significance should not be understated), solar system prices have halved in two years.

Yet while further dramatic cost reductions are expected in coming years, the coincident wind-back of Federal and state solar subsidies has left the Australian solar industry in a precarious position. In spite of this, opportunity remains for strategic solar companies to successfully maintain leading positions in preparation for an impending solar revolution.

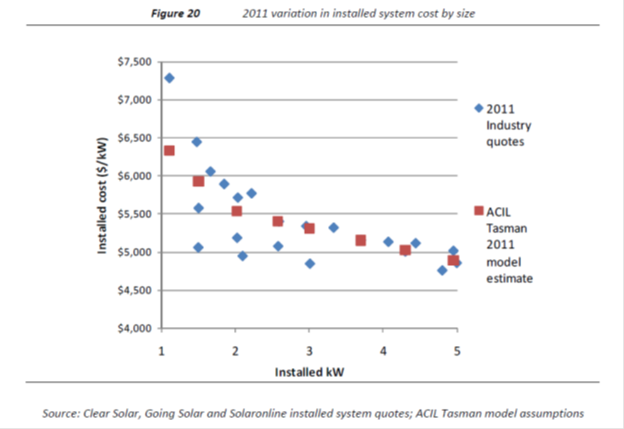

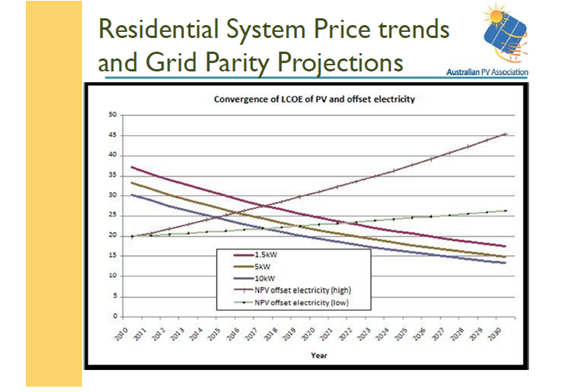

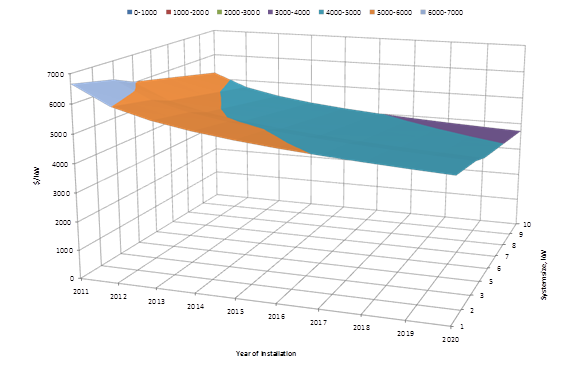

Since 1997, Australian photovoltaic (PV) system prices ranged between $10–14/Watt (W), averaging $12/W. According to an Australian PV Association industry survey , the average system price has halved in 2010 to $6/W. The 2011 pre-subsidy price of 1.5 kilowatt (kW) solar power systems remains close to $6/W, although economies of scale in inverters and installation means that the price of 5 kW systems is already below $5/W .

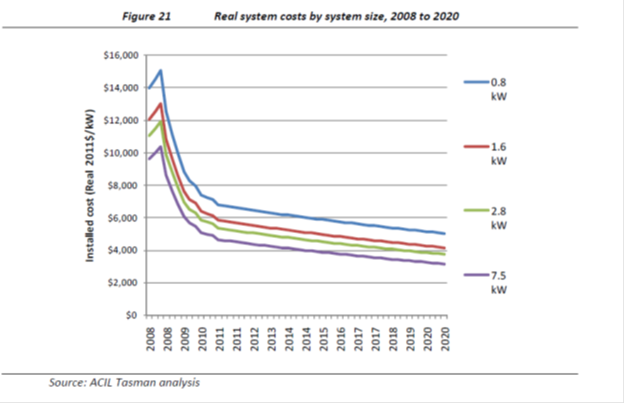

The $4/W barrier will be reached by 2014 for larger systems and in 2020 for smaller systems. This is significant because it corresponds with conditions in which solar power will then be generated at costs corresponding to those of regular consumer electricity tariffs, the exact timing of this ‘grid parity’ occurrence depends upon relative prices of retail electricity and solar installations. History shows that consumer solar demand is massive given favourable financial return, so solar becoming a mainstream energy choice is inevitable, though there are still many obstacles to clear first.

Rising sun, falling subsidy

Just as government support facilitated solar industry growth and its recent boom, so the retraction of government support threatens to undermine the solar industry, potentially wasting much of the industry development that has been achieved to date. Whereas both the Solar Homes and Communities Program and Solar Credits initiatives initially discounted system costs by approximately 67 per cent, the Federal subsidy has been slashed by an early reduction in the solar multiplier combined with a small-scale technology certificate (STC) price less than half the originally intended value of $40.

Combined, these factors have seen the Federal Government’s upfront support levels drop by 70 per cent in the space of four months. Customers that may have paid as little as $2,800 for a 1.5 kW system now face the prospect of forking out more than twice this amount. Rather than a predictably smooth transition, yet another solar policy instrument has proven unable to respond quickly or adequately to changing market dynamics, especially in light of significant state and Federal government policy interactions.

It now seems that most state governments are hitting the brakes at the same time, with the emergency stop leaving many in the solar industry with whiplash. Exporting power to the grid, once rewarded by premium net feed-in tariffs, has more recently been punished by regulations (or lack thereof) that set the price of exported power below the present or near-future retail tariff rate.

The New South Wales Government cut its feed-in tariff from 60 cents to 20 cents, followed by an extended period of uncertainty in which voluntary retailer contributions of 6 cents per kilowatt hour (kWh) were applied to exported power. Western Australia cut back its feed-in tariff to 20 cents/kWh (27 cents/kWh when combined with the State’s Renewable Energy Buyback Scheme), while South Australia cut its feed-in tariff from 44 cents to 22 cents. Extended interim periods in South Australia and Western Australia may stave off industry meltdown, but only Queensland is likely to be left with a significant premium tariff at year’s end.– SunWiz

Impact

The impact of Federal and state government solar funding cutbacks has been dramatic. Whereas a payback in less than eight years was easily achievable for most solar applicants in February 2011, the subsequent drastic reduction in STC and feed-in tariffs value means that one might now be lucky to obtain sub-ten year payback, at least without drastic reductions in input costs . Even ensuring solar generation receives the same price as the standard retail tariff doesn’t provide any reasonable payback, at least until the STC price recovers.

Interestingly, the reduced STC value means that economies of scale for larger systems balance the distortive influence of the 1.5 kW-focused solar multiplier. Though some of the market will opt for larger systems to achieve greater reductions in electricity bills, the economics of PV have soured across the board, and the sub-$3,000 systems that might have been paid from householders’ disposable income have evaporated. Such outcomes could reduce installations by 65–75 per cent according to ACIL Tasman modelling for the South Australian government.

Perhaps only prolonging the pain, hope remains for a brief reprieve. Most analysts predict that PV panel prices will fall substantially in the second half of 2011, as recently-constructed Chinese manufacturing capacity comes online, and Australian wholesale competition for a declining market intensifies. Panel prices from manufacturers with less than three years operating experience had already hit $US1.30 in June, which exerts pressure upon pre-established players.

Discusssions at Intersolar suggested prices would decline from €1.68 in the second quarter to €1.30 in the third quarter for European panels and $US1.72 to $US1.40 in the same time-frame for long-established Chinese panels. A further 3 per cent decline is expected by December, before a 6–8 per cent annual price trajectory resumes. However, even such dramatic decreases look unlikely to prop up the Australian PV industry.

Strategies

With the solar gold rush now in its dwindling days, market exits are expected – both voluntary and due to insolvency. It’s become a waiting game for many, with plenty holding onto STCs in the hope of a price recovery, though some degree of attrition is unavoidable. Strategic solar companies are more likely to survive by identifying innovative ways to package and deliver solar power, with resources targeted towards servicing more favourable markets.

For example, SunWiz has analysed recently-released postcode-level installation data to identify solar hot spots – locations and demographics with more favourable solar uptake and larger system sizes. Analysis of solar hot spots for individual solar companies may be able to identify more profitable target markets that can assist in navigating the market turbulence that lies ahead, and bridge the gulf between yesterday’s solar economics and those in the grid-parity future.

This article first appeared in Solar Australia, a quarterly magazine that covers important developments in the Australian solar energy industry, provides updates on new technology, project and policy developments. The publishers of Solar Australia – Great Southern Press – have been publishing EcoGeneration, Australia’s largest energy industry magazine, for many years.