Australian Solar Rides the Bull – More PV Installed in 2009 than Spain, and Set to Double in 2010

A report on Australian PV Market Share by SunWiz Consulting. A compilation of statistics from SunWiz’s Australian PV Market Insights

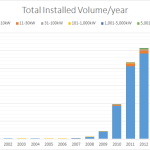

While the rest of the world stagnated during the Global Financial Crisis, one Australian ‘Bull Market’ bucked international trends to quadruple in size. Over 82 MW of PV was installed in Australia in 2009, more than the Spanish solar matador’s 70 MW of PV installations[1], and July 2010’s figures indicate that the Australian PV market will double this year.

Installations in the past twelve months have been supported by two federal government support schemes. Prior to the conclusion of the Solar Homes and Communities Program in June 2009, a 1 kW PV system received a $8000 rebate, plus approximately $1000 worth of Renewable Energy Credits. While a backlog of 60,000+ rebate pre-approved systems were being installed, the Solar Credits scheme supported new sales and installations.

The question on everybody’s lips this time last year was “How will Australian PV fare under the new scheme?” The answer is clear – installations supported by solar credits have grown steadily to now represent the majority of installations. This is remarkable, given the unstable nature of the support provided by Solar Credits, which represent a multiplied number of Renewable Energy Certificates (RECs) on the first 1.5kW of system capacity. As the REC price fell to below $30, so too the value of solar credits plunged to approximately $4600 discount on a 1.5 kW system. However, a strong Australian dollar and international oversupply of PV panels, combined with a REC-price rebound upon government announcement of a review of the support mechanism for PV meant that installations have grown steadily.

Australia’s PV industry is notable for the predominance of small residential systems. Strongly influenced by the structure of government support, the vast majority of systems were of 1 kW in size under the rebate. The immediate effect of the Solar Credits scheme was to increase the average system size to 1.5kW, though many more 2kW and 3kW systems were sold than previously.

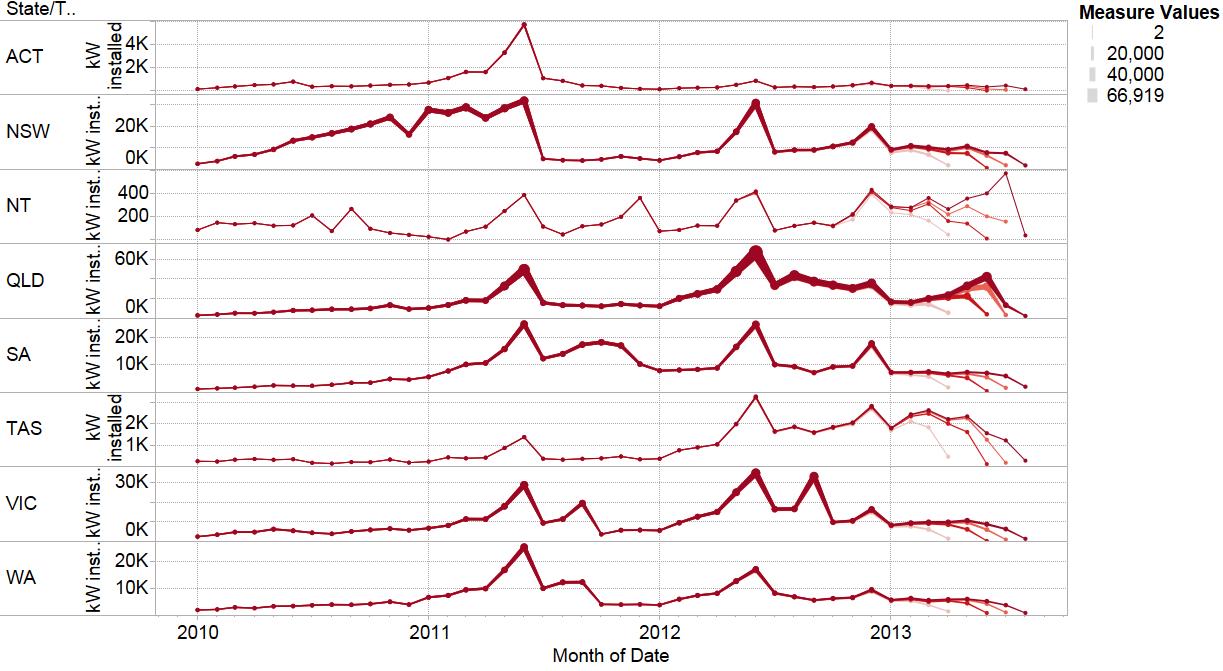

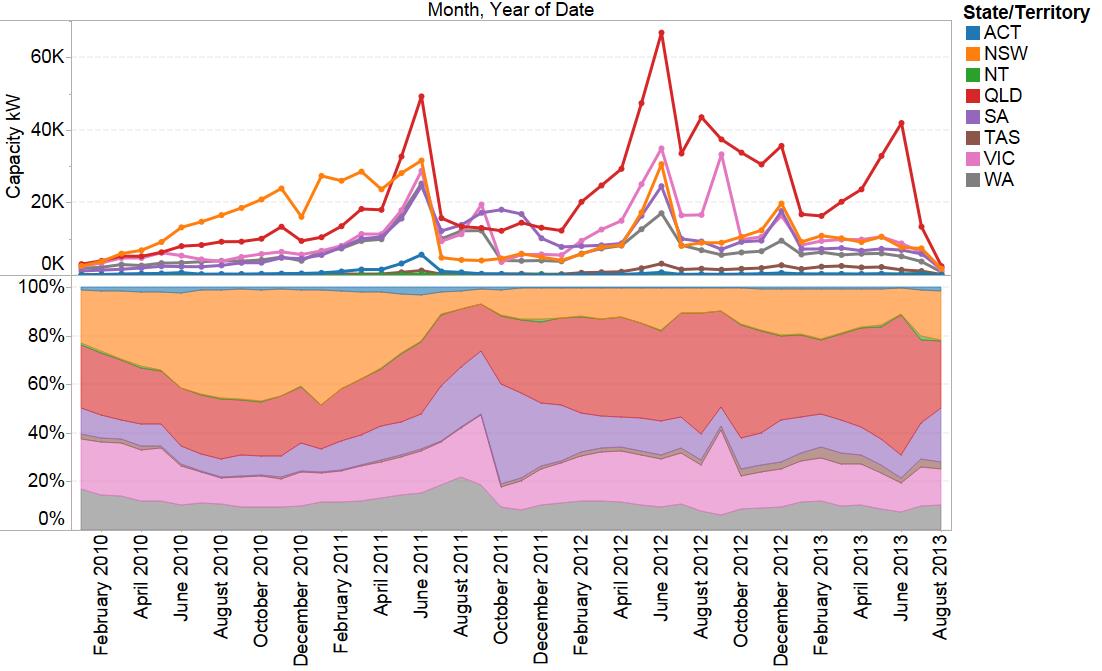

In spite of some predictions for market consolidation, the Australian market has become increasingly competitive. Many new entrants have displaced more established companies, with the top 10 ranks shifting considerably. Victoria has hosted some of the most successful solar upstarts, who now strongly dominate that state, though the larger markets of Queensland and New South Wales are more hotly contested.

State-based Feed-in Tariffs provide some degree certainty to solar industry. The New South Wales market has grown rapidly on the back of the gross feed in tariff, which is now due for review. States with less generous net Feed-in Tariffs have also grown steadily, albeit at a slower rate.

What does the Future Hold?

Although well on its way to 200 MW of installation this year, the backlog of rebate-supported installations will have been fully installed by the start of August. This means that 36% of last month’s installations will dry up overnight. This could mean Australia falls short of 200 MW of installation this year. However, with 43 MW of rebate-supported systems plus over 53 MW of solar credit systems installed in the first half of the year, at least 149 MW should be installed if solar credit system installation continues at the same rate. However, recent amendments to PV’s support scheme could substantially change this forecast.

In recognition of renewable energy industry concerns that small-scale systems were cannibalising other large scale renewable energy technologies, the Australian Parliament recently passed amendments to the Renewable Energy Target. These create unlimited demand for small-scale RECs, and a fixed $40 REC price from 1/1/2010. This would have led to greater certainty for the PV industry, were it not for last minute amendments to the scheme.

The Enhanced Renewable Energy Target (eRET)[2] now allows for an annual adjustment to the $40 REC price. This in itself is no less stable than the previous floating REC price, though more prone to political agendas than the original market-based scheme (even with its flaws). However, the government minister can now reduce the solar multiplier in advance of its legislated reduction on 1/7/2012, and thus drastically reduce the discount on the upfront cost of PV systems. A possibility also exists that the Regulator will increase the system size that benefits from the solar multiplier to 3 kW. SunWiz will release detailed analysis of the impact of the new eRET next week – stay tuned.