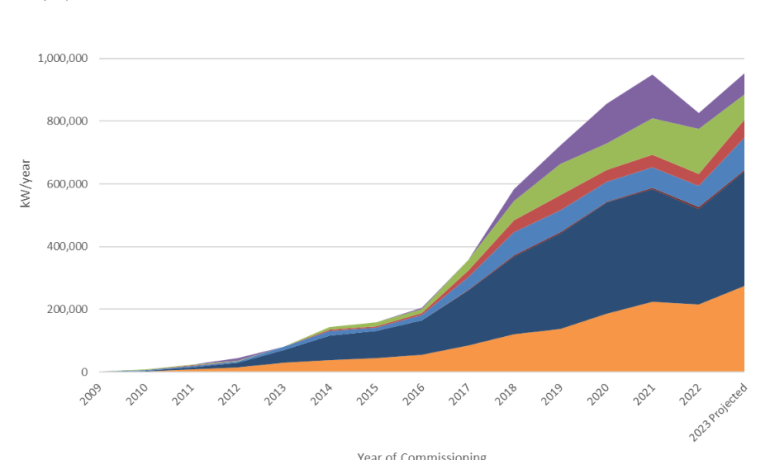

4.6GW of PV installed in Australia in 2023

Courtesy of the REC Registry, SunWiz provides accurate and timely reports on the STC market in the first week of every month.

But data on non-STC systems isn’t as easily compiled. Throughout the year, SunWiz identifies large commercial projects on linkedIn, project portfolios on retailers’ websites, the LGC Registry, VEECs, and more. At the end of the year, SunWiz receives commercial project lists from participating retailers, which we verify and validate to ensure systems are legitimate and not double-counted. We also check which solar farms started generating power that year.

To ensure our data is as accurate as possible, we also adjust our calculations for Victorian installations that clearly occur outside of REC Zone 4.

We then true-up data to account for typical lag in STC & LGC reporting, to provide figures based upon date of installation/commissioning (as opposed to date of certificate creation).

On this basis, SunWiz is pleased to announce 4.3GW of capacity was installed/energized in 2023. Here’s how that breaks down into segments:

2023: Australia’s first year of contraction since 2013

4.6GW of solar power is an impressive annual installation figure that will keep Australia on the global stage of leading solar nations.

However it’s far less PV capacity than was installed in recent years. In fact, this was Australia’s worst year since 2019. It was also the first year the Australian PV industry contracted since 2013.

| Segment | Capacity (MW) |

|---|---|

| Residential | 2,526 |

| 15-100kW | 640 |

| 101-5000kW | 245 |

| 5-20MW | 103 |

| 20-100MW | 129 |

| 100MW+ | 933 |

| Total | 4,578 |

Why the Australian PV industry contracted in 2023

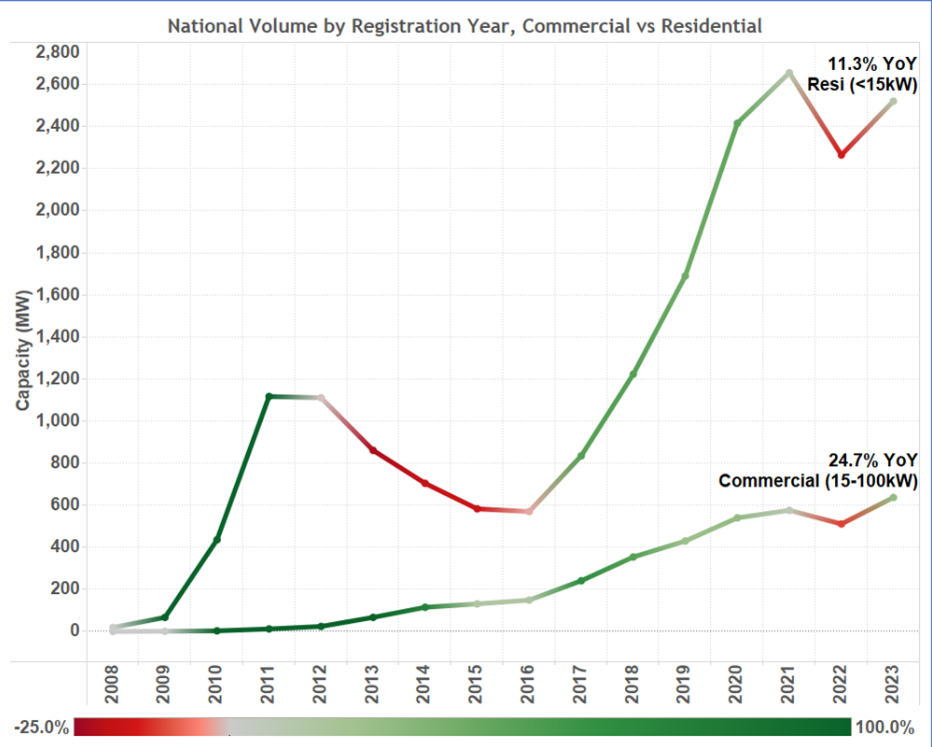

The 2023 Australian PV industry contraction occurred despite the success of the residential segment – which grew by 11% (2023 vs 2022 installation year) to post a second-best year on record – and the sub-100kW commercial market – which grew by 23% to reach a new record.

The contraction didn’t occur because of commercial systems sized between 101kW-10MW, as that segment increased by 15% and set a new record.

The real reason the Australian PV market contracted in 2023, despite the success of rooftop PV systems, was because of the big contraction in energization of new solar farms. That 1.1GW worth of systems larger than 10MW energized in 2023 compares to 2.9GW in 2022. This was the net result of a decade of inaction and blocking by the previous federal government that caused development of solar farms to stall, once the Renewable Energy Target was met.

Why rooftop PV must be accelerated

The rollout of low-cost bulk power from solar and wind farms is essential for the future of Australia’s decarbonisation efforts. However, the solar farm pipeline has backed up, with SunWiz analysis showing only a modest increase in solar farm energization will occur in 2024.

It could take years of high electricity prices before new-build solar & wind farms again put downward pressure on wholesale prices. In today’s economic climate, high electricity prices put the energy transition at risk of losing its social license. While we build momentum for solar & wind farm construction, we should be accelerating the rollout of rooftop PV.

Here’s our key recommendations:

- Rather than continually decrease support for PV (as is currently baked into the annual reduction of the STC deeming period), the STC deeming period should be frozen at current levels for 3 years.

- While verifying projects, we noticed many that had initially installed 100kW were now coming back to add more power, in many cases tripling in size. The 100kW STC cap was put in place when such systems were rare. Now that artificial cap creates arbitrary limits on system sizes, and influences behaviour so that businesses aren’t putting on the system size they truly need. By adopting the Capacity Investment Scheme rather than extending the Renewable Energy Target, it makes even less sense for businesses to install costly metering equipment in order to create LGCs. Extending the STC threshold to 1000kW will remove the red tape on green businesses.

- PV should be made mandatory on new warehouses & factories. While verifying projects, we noticed how many commercial PV systems were going up on newly built factories and warehouses. This makes sense, and should be mandated.

- Batteries should be incentivized. Home energy storage systems facilitate greater uptake of PV systems, by freeing up network capacity and because the lead to higher feed-in tariffs and lower prices of imported electricity.

- Networks should be forced to meet voltage requirements. Far too much of the distribution network is run at higher-than-regulated voltages. Reducing those voltages increases the hosting capacity of the network.

- Shift all remotely-operated ‘off-peak’ electric hot water devices to daytime consumption. Soaking up that energy produced by solar power during will increase networks’ hosting capacity.

Australia’s PV success story wouldn’t have happened without rooftop PV, which makes up over two-thirds of Australia’s deployed solar power. Residential PV is 50% of Australia’s total PV capacity. While we remove obstacles and again build momentum in the rollout of solar farms, it’s time to back rooftop solar.