3GW of Australian PV- When Where and How

Also in this series: Australian PV Contribution reaches 9.4% of electricity demand

3GW of PV – When, where and how: System sizing, pricing, and distribution

3GW of PV – which companies are leading residential and commercial PV

When and where and how did 3GW of PV get installed? System Sizes, Pricing, and Distribution

Email not displaying properly? View it in your browser.

3GW PV Size and Shape

Yesterday in our free Insights mini-series edition, we saw how PV provided nearly 10% of midday power consumption across the NEM on September 29, and looked at regional solar coincident performance. Today we’re going to see the size and shape of the PV industry, (whose great volatility and quickly-emerging trends makes monthly tracking invaluable). Remember, this release of Insights data is a once-off to celebrate the 3GW milestone. To access this data regularly, you’ll need to subscribe (from $275/month)

The graph above shows the peaks and troughs that the solar industry experienced over the 2010-2012 period. The national (black) and state (coloured) lines indicate how the monthly installation figures in response to multiplier reductions and state feed-in tariff reductions. The precipitous plunge that resulted from the end of the FiT in NSW was followed by a very quiet second half of 2012, before installations started growing again of their own accord: smooth organic growth punctuated by peaks from multiplier reductions. Western Australia followed similar form but without the same recovery. Feed-in tariff closures proved equally as important as multiplier reductions in driving installation booms, as clearly shown in peak installation levels in Victoria and South Australia. Looking across the country, its clear why this period was known as a “solar coaster”.

Thankfully things have stabilised considerably in the past year. As system registration lags behind installation, it can take some months to obtain a clear picture of recent installation trends. SunWiz has created a calculator that projects recent installation volume from current registration activity. The graph below shows the expected monthly installation volume for the most recent year, compared to finalised data for the year before. Clearly 2013 is more stable; absent are the signature peaks of multiplier reductions. Queensland’s installation surge resulting from the completion of its 44c feed-in tariff is the main anomaly in otherwise steady installation levels, though South Australia is having a final surge as its feed-in tariff closes. Absent these factors, 50-60MW/month seems to be a consistent volume of installations. Subscribers to Insightsreceive monthly updates on registration volume by state, which helps them track market share.

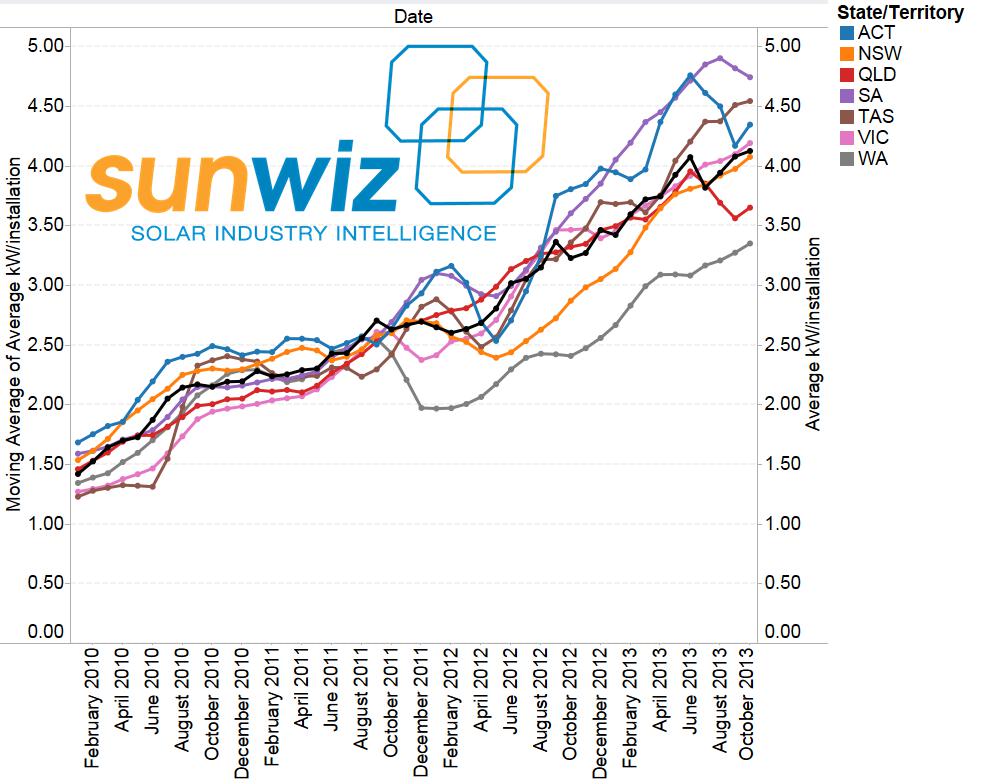

The average system is growing in size too, to the point where the average system is now 4kW in capacity. The graph below shows average system size by month for each state (colour; smoothed) and nationally (black). When feed-in tariffs were removed in WA and NSW, the average system size fell markedly. However, since that point the average in these states as grown in parallel with the national average. NSW now sits in line with the national average (though this is because NSW is the most successful market for commercial PV, which it was forced to focus upon earlier than in other states due to the lack of feed-in tariff for residential systems), and WA is far behind. Since Queensland’s feed-in tariff installations were completed, average system size has declined markedly as there is no longer a 44c/kWh incentive to export power. Meanwhile average system sizes are currently high in Tasmania and South Australia, both of whom presently enjoy feed-in tariffs, though SA is also starting to fall back. Subscribers to Insights receive monthly information on average system size.

A major reason that customers have been buying larger systems is their steadily-improving economy. The graph below shows the evolution of the net price (after STC discount) and calculated gross price (before STC discount) in terms of $/W for a range of system sizes of PV retailers that list prices through Solar Choice. More recent months are shown in darker blue, with the most recent month shown in pink. It can be seen that the gross price has near-continually declined over time, and that there is an appreciable economy of scale for larger systems. Net system prices have varied more as the solar multiplier was eliminated and as the STC price recovered. The average net price of a 5kW system has thus fallen by one-third from $12500/W in mid 2012 to $8000 today. Subscribers to Insights receive monthly updates on system prices by size, state, and quality of components.

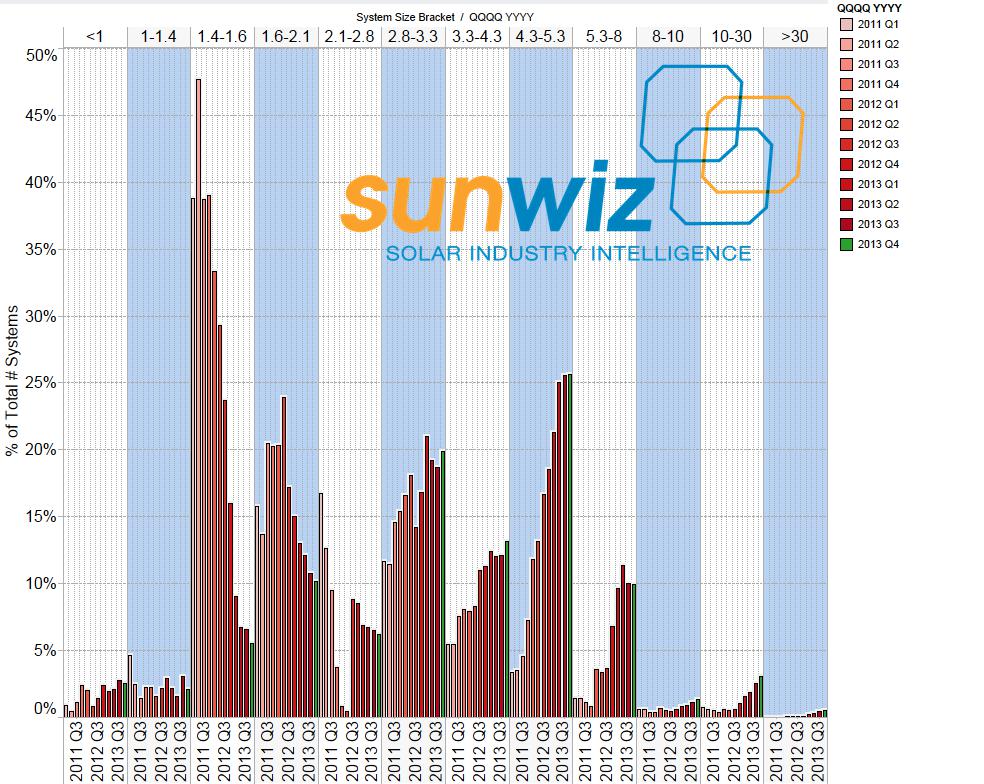

Over this time the nature of solar installations has also shifted considerably. The national distribution of system sizes by quarter shown below reveals the earlier popularity of 1.5kW systems is now more focussed upon 5kW systems. At one point, half of all systems installed were 1.5kW in size. Most recently 25% have been 5kW in size. However, the shift towards larger residential systems seems to have plateaued. The proportion of 3kW, 4kW, and 5kW systems has been steady for almost a year; what we’re seeing now is the emergence of a market for commercial solar. 3% of systems installed recently are in the 10-30kW range, but 10% of volume (by kW) falls into this range, plus another 7% in the 30+kW range. Considering that in 2012 only 5% of capacity exceeded 10kW in size (and a lot of that was driven by solar schools and feed-in tariffs), we’re finally seeing a remarkable shift towards commercial PV in Australia. Subscribers to Insights receive monthly updates on the distribution of system sizes by state.

This information regularly appears in the Insights subscription. Still to come in this mini-series, we will look atlarge-scale systems, market share, and SunWiz-exclusive content. Pricing insights are drawn from information and data provided by Solar Choice to SunWiz. Solar Choice Commercial impartially manages a large diversity of tenders for solar farms and commercial PV, and has energised some of Australia’s largest roll outs. Solar Choice Residential has assisted over 50,000 households to make a well informed selection of installer. Solar Choice has unique software to deliver objective, informative and immediate Quote Comparisons to the market, and follows through to broker and deliver installation contracts and deposit payments to its network of reputable installers.

Want more information? Subscribe to Insights

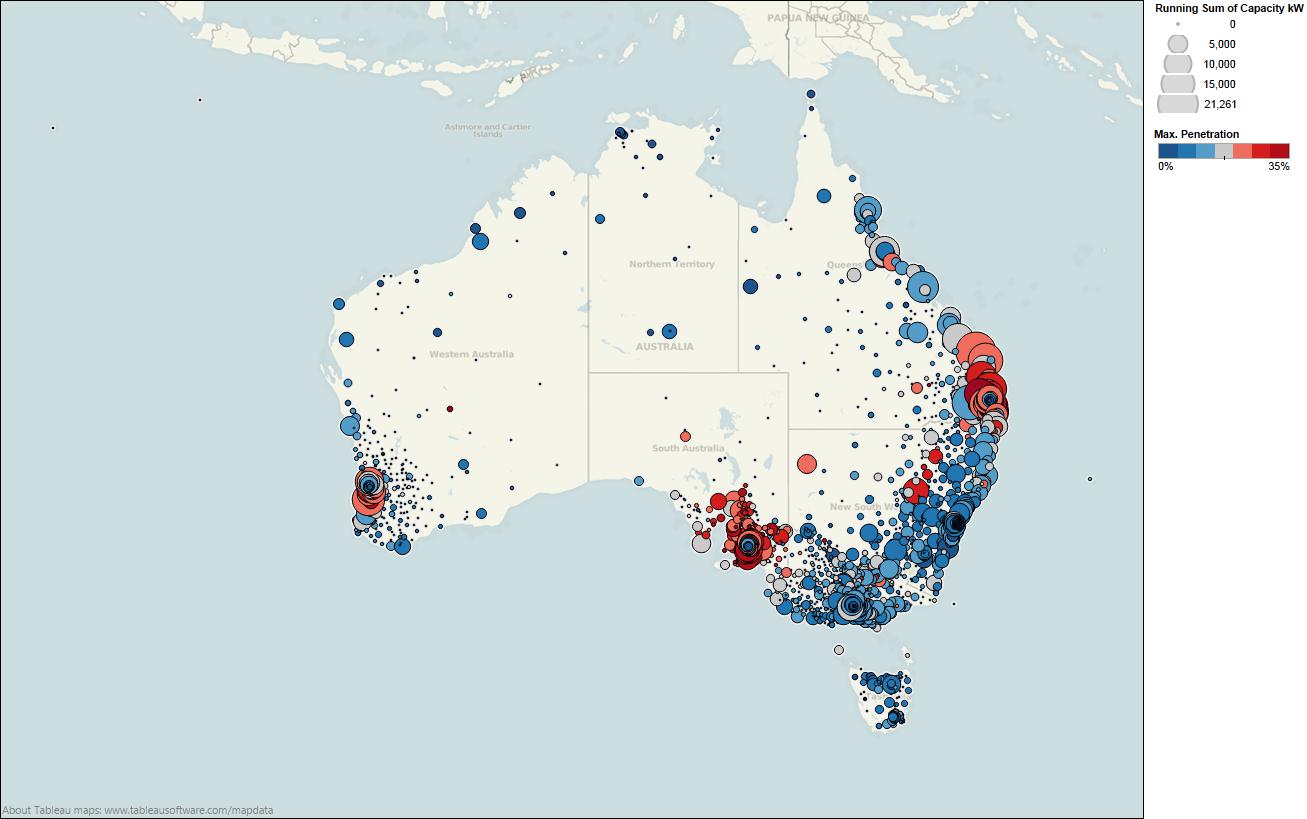

Where has it ended up? The map below shows the total installed capacity by postcode (size of dot) and the proportion of total dwellings that have solar power. The greatest volume of solar power lies along the Queensland coast. There is clearly highest penetration in South Australia and South-east Queensland, though the area surrounding Perth also has a high solar density. Installations are naturally concentrated in capital cities, though there is greater geographic spread of solar in Victoria and New South Wales.Subscribers to Insights receive an overview of solar hot spots.

Insights into Insights

Insights is subscribed to by most of the top players in the Australian PV Industry. This includes 11 of Australia’s PV Retailers (including each of the top 4 plus major solar utilities), 6 of the top PV Wholesalers, and eight of the major PV component manufacturers. If you’re creating STCs for yourself, it’s likely that they know more about your business that you realise. And if you’re not self-creating STCs, you can fly under the radar while performing espionage on their strategies.

Here’s a description of what’s included in each subscription level.

| Inclusion: | Standard | Premium | CustomID |

| Track market share, identify emerging trends, enhance success | X | X | X |

| Perform SWOT analysis on market leaders incl recent growth/contraction | X | X | |

| Identify, Evaluate, and Monitor Customers. Manage Debtor Risk | X | ||

| Australian PV market monthly capacity & #systems registered – nationally and by state | X | X | X |

| Evolution of average system sizes – nationally and by state. | X | X | X |

| Distribution of system sizes – most recent month | X | X | X |

| Solar Choice Market Insights: system pricing analysis | X | X | X |

| Rotating Feature: Market Share (National Top 20, State top 10) for current year (Interactive) / Large Scale PV Market / Feature Installer | X | X | X |

| Special Feature each month | X | X | X |

| Data table of: Total Capacity by Installation Year & Registration Month – state & national, Average system sizes, Popular system sizes for current year, Market share (top 20 nationally, top 10 in each state) for current year, quarterly rankings (top 30 nationally), #systems by size by date. | X | X | X |

| Premium Data Table: Top 50 nationally & Top 20 in each state – #installations & installed capacity by month for current year | X | X | |

| Premium Data Table: Distribution of system sizes for current year for top 50 nationally. | X | X | |

| Interactive Graph: Players experiencing Growth and Contraction | X | X | |

| Interactive CustomID Inspect key statistics of top 200 players nationally |

To learn more about what we can do for your solar business

Latest Tweets

- Great guerilla marketing photos of solar power… http://t.co/KGyiRy8Wfm9:14AM

- ZEN Energy and Business SA partner to provide commercial solar over 5-7 year rental planhttp://t.co/ty4hdOnJhj2:28PM

- SunWiz was featured in The Courier Mail: Solar panels turn suburban homes into QLD’s fourth biggest power station http://t.co/q4eEOr3Xm21:25PM

- RT @The_RiotACT: Three new power plants for you: Photon Energy are planning to build three mid-sized solar power plan… http://t.co/Fd2OJR…1:03PM

- RT @ClimateSpec: EDIS: Campbell Newman’s electricity tax by stealth http://t.co/yH5mJHoZgI1:00PM

- APVI study explained: from base case of $1735/year electricity spend, installing an AC will raise your spend to… http://t.co/6AXlEEMYIo10:28AM

- APVI: PV systems producing 20% of capacity during local distribution network peak demandhttp://t.co/Tb0I4DIKKI10:22AM

- SunWiz leads ClimateSpectator – who’s leading commercial markets. Great graphs (even if I do say so myself…)… http://t.co/47jZhKMzS210:21AM

- AEMO: 13% of additional generation to 2020 will be solar PV… http://t.co/qK4Rdumere10:19AM

- Time to get facts right on solar, and reap the benefits – Centre for Policy Development and APVIhttp://t.co/l3NCvMfAmF10:16AM

- RT @renew_economy: CEFC saved in the Senate – a rare win for Australian renewableshttp://t.co/nZfdcBCJ8l #solar #wind1:59PM

- RT @SimonChapman6: God takes a selfie http://t.co/664s5ZIRUJ1:57PM

Latest Posts

Great guerilla marketing photos of solar powerhttp://www.renewableenergyworld.com/rea/blog/post/2013/12/solar-freds-top-solar-marketing-wishes-for-2014-in-pictures?page=all[see more]12/16/13 9:14AM

Great guerilla marketing photos of solar powerhttp://www.renewableenergyworld.com/rea/blog/post/2013/12/solar-freds-top-solar-marketing-wishes-for-2014-in-pictures?page=all[see more]12/16/13 9:14AM APVI study explained: from base case of $1735/year electricity spend, installing an AC will raise your spend to $1977 when network impact is costed, and will raise non-AC users bill to $1818. Assuming the AC has been installed, installing PV will reduce your bill from $1735 to $1373, and will reduce other customers bills by $19. http://www.businessspectator.com.au/article/2013/12/12/solar-energy/solar-no-freeloader?utm_source=exact&utm_medium=email&utm_content=544618&utm_campaign=cs_daily&modapt=[see more]12/13/13 10:28AM

APVI study explained: from base case of $1735/year electricity spend, installing an AC will raise your spend to $1977 when network impact is costed, and will raise non-AC users bill to $1818. Assuming the AC has been installed, installing PV will reduce your bill from $1735 to $1373, and will reduce other customers bills by $19. http://www.businessspectator.com.au/article/2013/12/12/solar-energy/solar-no-freeloader?utm_source=exact&utm_medium=email&utm_content=544618&utm_campaign=cs_daily&modapt=[see more]12/13/13 10:28AM- SunWiz leads ClimateSpectator – who’s leading commercial markets. Great graphs (even if I do say so myself…) http://reneweconomy.com.au/2013/solar-success-whos-leading-residential-commercial-markets-41870[see more]12/13/13 10:21AM

- AEMO: 13% of additional generation to 2020 will be solar PVhttp://reneweconomy.com.au/2013/aemo-sees-coal-sidelined-as-renewables-dominate-new-capacity-19726[see more]12/13/13 10:19AM

A Big Week for SunWiz – thrilled to have reached 2222 people via Facebook alone![see more]12/12/13 10:24AM

A Big Week for SunWiz – thrilled to have reached 2222 people via Facebook alone![see more]12/12/13 10:24AM