2019: Rooftop Solar fills the gap left by slowing Solar Farm deployment

SunWiz has already reported the impressive growth of rooftop solar market in the sub-100kW segment. Now SunWiz has completed its tally of systems larger than 100kW to reveal the annual solar tally for 2019.

It’s worth briefly recapping the highlights of 2019 in the sub-100kW space:

- 2.13GW of sub-100kW installed in Australia in 2019, a record level

- 35% growth over 2018 figures

- 3x the volume installed just three years ago

- Record annual tally in every mainland state and territory

- A cumulative 10GW of sub-100kW installations

- Snowball vs Saturation: Some of the postcodes in Australia’s Top 20 postcodes are growing 4x faster than the average postcode

- Residential Return: 2019 was the first year in a long time that the residential market kept pace with the rate of growth in the commercial market

- Prices at Record Lows: System prices continue to fall, though not as fast as in previous years.

- Small Commercial is the new black: The 10-20kW market is growing fastest in percentage terms, as companies typically in the residential leaderboard master this market segment.

- Top Retailers Growing Rapidly: Most of the top 20 retailers in the sub-100kW market had record years. One top-10 company grew by >250%.

- NSW #1 again: New South Wales remains the leading state for sub-100kW installations

- Network limiting system size: 6.6kW systems are the most popular size by a long margin. For now, they’re also effectively the maximum size permitted by many networks on a single-phase connection.

- This year, 363 solar LGC systems were installed, totalling at least 1.46GW.

- Many of the companies that were previously successful in the sub-100kW commercial market have grown in size and scale, and now do far more volume in the >100kW market.

- This success in commercial installations now means some companies rank higher than most residential installers. The #3 company for rooftop solar installed 50% more capacity in the LGC market than in the STC market, and the #7 company for rooftop solar installed 200%.

- Despite commercial success for some companies, the volume of commercial installations hasn’t grown much in 2019, with the exception of the 1-5MW category.

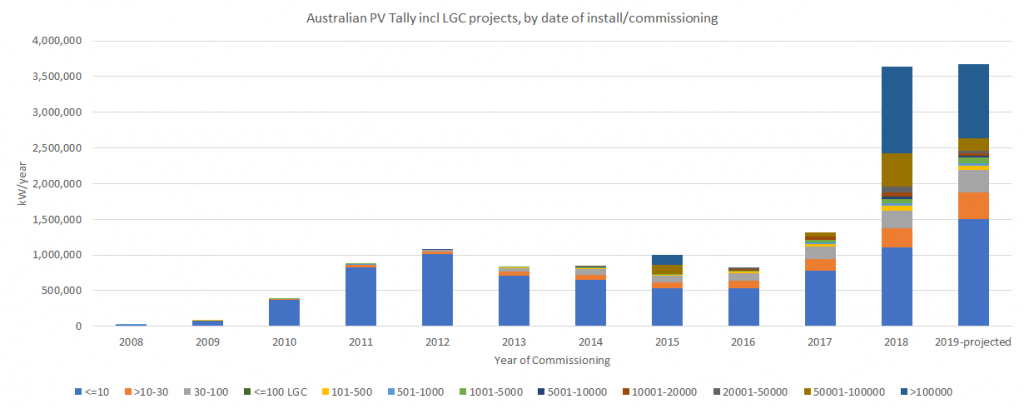

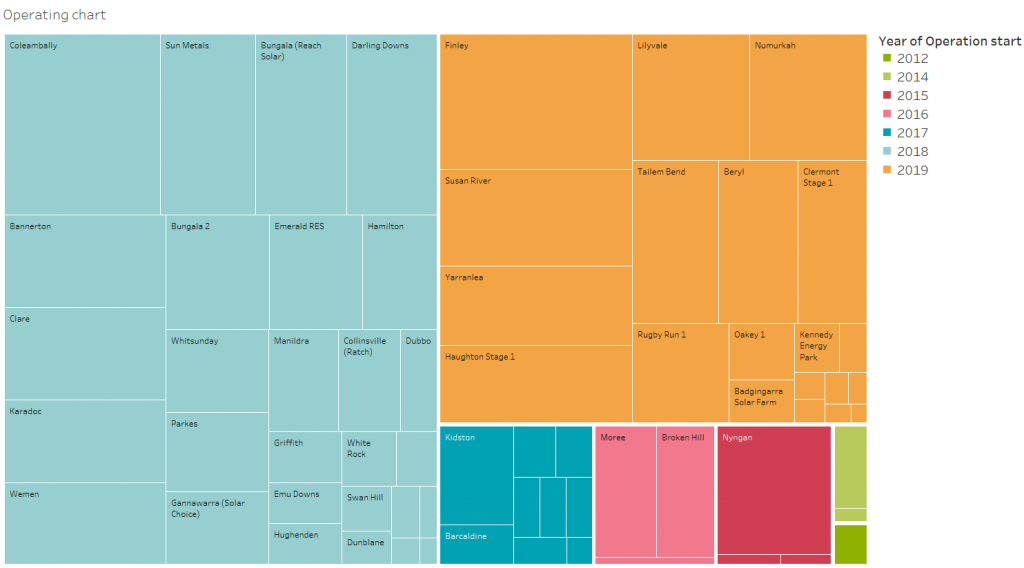

- As illustrated below, the capacity of Solar Farms commissioned in 2019 has fallen considerably, for reasons that include contractor disputes, lawsuits, economic woes of EPCs, grid connection hold-ups, synchronous condensers, MLF adjustments, curtailment, and negative wholesale power prices (as extensively documented in RenewEconomy).

- Solar Farms exceeding 10MW in size fell by 30% to 1.3GW in 2019, down from 1.8GW in 2018,

When you tally it all together you get a market that is 1% bigger than in 2019. This illustrates that in 2019 the rooftop solar market (in particular residential and small commercial) has filled the gap left by solar farms. It’s worth noting that SunWiz has made adjustments for lag in registering installations with the Clean Energy Regulator, along the lines of typical lag factors from previous years.

SunWiz’s 2019 Year In Review gathers the full solar PV market data of 2019 and transforms it into a powerful, insightful and strategically crucial document for any solar business.