2018 – Top PV Retailers

By all accounts, 2018 was a stellar year for Australian Solar Power. To celebrate all of the solar glory, SunWiz has written a series of articles covering 2018 – the key trends, achievements, and milestones for each state and segment of the Australian solar industry. These trends, facts and figures are covered in extraordinary detail in SunWiz’s 2018 Year in Review, which can be purchased for $1995 ex GST, which also includes a complimentary 3 month subscription to Insights, SunWiz’s flagship PV market intelligence subscription.

The topics covered in our Year in Review series are:

- 2018 – Australia’s record breaking year. In eyewatering charts

- 2018 – state roundup

- 2018’s Top Retailers

- 2018 – Trends in Commercial PV

- 2018 – residential revival

- 2018- Australia’s magnificent year for solar farms

Top PV Retailer by volume in each segment:

SunWiz tracks every individual installation in the Australian market, based upon STC and LGC creation. Most of the largest companies self-register STCs, which provides highly granular and accurate insight into the volumes of the players that make up the top ranks. Our full Year in Review report provides the annual and monthly volumes for the top players in the national STC market, plus the annual volumes of the top players by state and in each commercial size segment in the STC market. Redacted versions of these charts are shown below, in order to identify the top player and the competitiveness of the state or market segment.

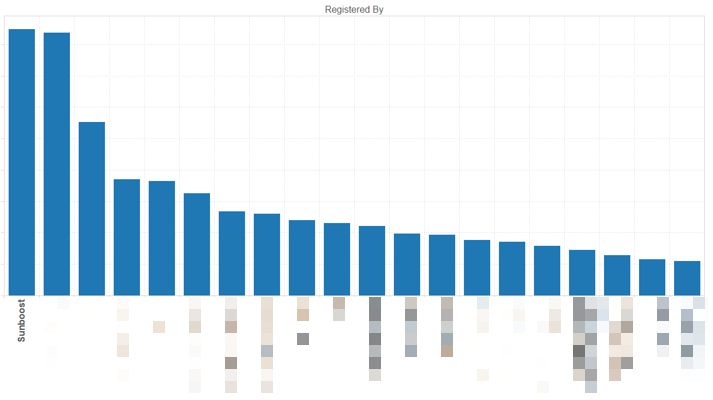

STC Market Overall:

Sunboost – who narrowly reached position #1 after growing rapidly over the year. The third-ranked player had two-thirds as much volume, and then it tailed off after that. Sunboost also was the #1 PV retailer for residential volume. It’s difficult to achieve national success: of the top 20 retailers for 2018, only a handful had substantial volume spread across 4 or more states. Being strong in one state can be enough to get into the top ranks nationally, but only four companies achieves a top-20 ranking predominantly from success in a single state. Most of the top 20 are therefore successful in more than one state, but haven’t yet nailed it in every state.

State Markets:

On a state-by-state basis, the top volume players were as shown below. In each of the ACT, NSW, NT, and QLD, the #1 player dominated that market. In contrast the #1 spot in both WA and TAS were closely contested, and the top ranks were more evenly distributed in VIC and SA. It was also the first time in many years that the #1 rank in each state/territory was a completely different company.

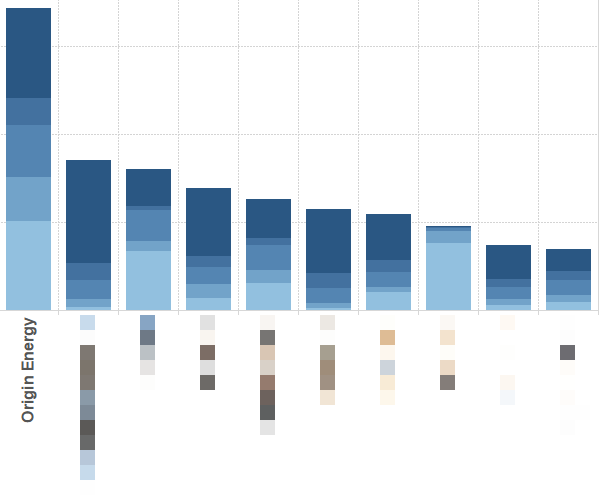

Commercial Market:

In the 10-100kW range of STC commercial PV, the #1 spot by a long margin was taken out by Origin.

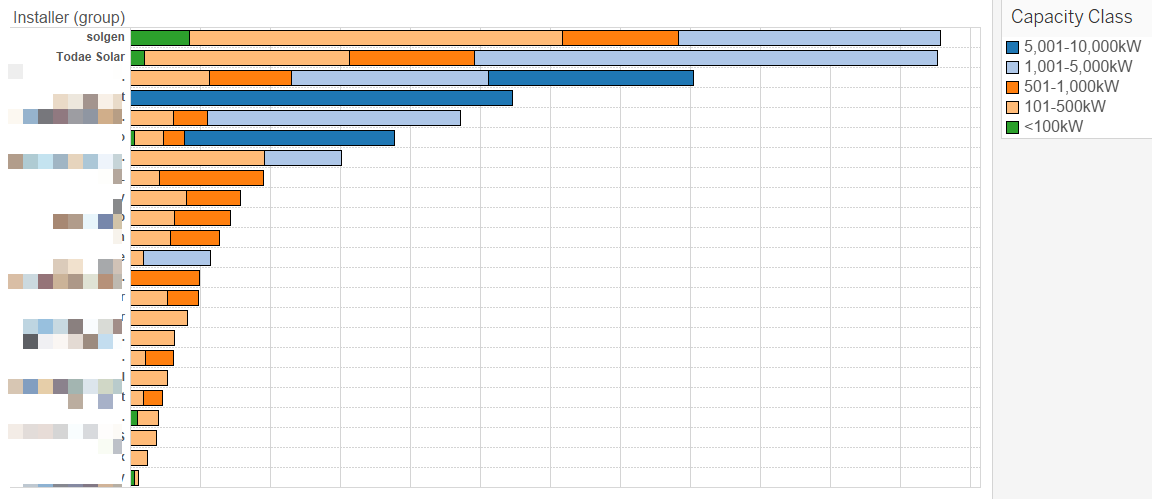

LGC market

The LGC market was almost too close to call. Solgen had the most volume of commercial LGC projects, by a small margin over Todae Solar. Because many of Solgen’s LGC installations were multiple buildings spread across a campus, Todae Solar were actually #1 for installations over 100kW. But when combined with commercial STC systems, Solgen also took out the coveted position of #1 commercial retailer overall.

2019 looks almost certain to exceed the records set in 2018. Rooftop PV continues to offer an unbeatable financial return, solar farms in construction exceed the capacity built to date, and state government programs are ramping up. To boost the solar industry this year, SunWiz has kicked off 2019 by including free high-definition rooftop imagery in every PVsell account, and offering a stand-alone roof layout tool for those who don’t need to use PVsell’s impressive financial analysis and tailored customer proposals. Both of these continue SunWiz’s mission to assist businesses to sell more solar for greater profitability.

Order your copy of the 2018 Australian PV Year in Review here.

Subscribe to PVsell and get high-definition rooftop imagery included at no extra charge.